When Fundamentals Aren’t Always the Deciding Factor

Two Sohn ideas that hinge on ownership and execution as much as valuation

One Thing Before We Begin

I wrote last week about the potential impact on the composition of the S&P500 of private companies floating. We have seen more commentary about a Space X IPO this week and I covered it in my socials:

I also listened to a podcast with Elon Musk (it’s disappeared from my queue, but I don't think you are missing anything) and one thing he said interested me. Asked about what he would invest in, he explained that AI and robotics would dwarf everything else in future:

“I don’t have like a portfolio or anything. So, I guess AI and robotics are going to be very important. So I suppose there would be AI and robotics that aren’t related to me. I think Google is going to be pretty valuable in the future. They’ve laid the groundwork for an immense amount of value creation from an AI standpoint.

NVIDIA is obvious at this point. I mean, there’s an argument that companies that do AI and robotics and maybe space flight are going to be overwhelmingly all the value, almost all the value. So the output of goods and services from AI and robotics is so high that it will dwarf everything else.”

Here is David George, a General Partner at Andreesen Horowitz, who runs the growth investing area, from an Invest like the Best interview, on the same theme:

“There were probably one or two technology companies in the largest 10 market cap companies in the world. Now it’s eight of 10 and seven of the eight are West Coast technology venture backed companies. That realization hasn’t really fully hit the finance industry.”

He went on:

“…if you look at that, tech has overtaken all of the market cap creation and is mostly driving force of the stock market and the economy. The private markets have become a real asset class…..turns out there’s 5 trillion of private market cap that is up 10X in the last 10 years. And it’s honestly some of the best companies in the world. That market cap represents almost a quarter of the entire S&P 500. It’s more than half of the Mag 7.”

And he pointed out that the private companies are growing more quickly:

“ we spend most of our time in software consumer and fintech stuff, the public universe in those sectors, there’s less than five companies growing 30%…..That’s a low number.…. if you look at the composition of small cap public companies, the quality, I would argue, is so much lower than what is available in the private markets.”

I read a lot about AI, almost everywhere. This aspect - that many of these companies will end up in public markets and change their shape - seems to get less attention. I shall return to it. Meanwhile, back to today’s world….

Introduction

This week, back to the Sohn Conference from November 2025, to pick up on some of the stocks presented. In this article, I highlight two really interesting stocks pitched there. With these conference reports, it’s always tricky to decide in which sequence to write up the stocks, as I am usually unfamiliar with the companies and don’t know the presenters.

I previously decided to write them up based on how interesting they seemed, which would push me towards the best presentations. Then I included a factor for subsequent performance, so I would be more inclined to write about stocks which had fallen. When I investigated, the worse performers didn’t always seem that much more attractive when the idea was more closely examined.

Hence I have now determined that the best strategy is to take requests – I shall publish all the ideas for premium subscribers following the conference and you can vote for the stocks you think are most interesting. Otherwise I shall publish based on

the presentation

how interesting and off the beaten path the idea seems

whether I can add any value

I amn’t going to discuss biotech stocks here, as I have no knowledge and I feel they are often binary – the drug works or it doesn’t. I also tend to avoid the most popular stocks unless I think there is an interesting angle. I would welcome readers’ input on this – I simply cannot write up 15 stocks in a week, even superficially.

One of the stocks this week is a European services company which has bounced significantly as bid rumours have swirled round it. It was pitched by Avi Fruchter, founder and CIO of Vintra Capital, a really astute investor with whom I had a coffee a couple of weeks ago.

Avi started out at Atticus Capital, a hedge fund which was highly successful in the mid-2000s, and later formed a fund with a partner, before setting up Vintra on his own. He is super smart and this was an extremely interesting idea which has a long way to go to recover its former peak, in spite of the bid rumours. But it’s a slightly more complicated story, as I shall explain.

The other is a German industrial which should benefit from infrastructure spending and is something of a turnaround story. It was pitched by Igor Kryca of Lombardi Capital, a hedge fund manager with 25 years of experience who specialises in finding undervalued durable assets undergoing transformation. He used to work for Scott Bessent at Soros, set up on his own in 2021 and now has over $500m AUM.

Again, I thought this was an interesting industrial – it’s a global leader in an essential component with a continuous need for spare parts; even better, these are safety critical systems. The stock had underperformed a lacklustre market since it was floated in the late 2010s and is higher quality than the market has given it credit for.

Aftermarket is over half the sales and 80% of the profit with a significant installed base. The company has had a series of management changes but now has a “real deal” CEO and Igor thinks it’s a double.

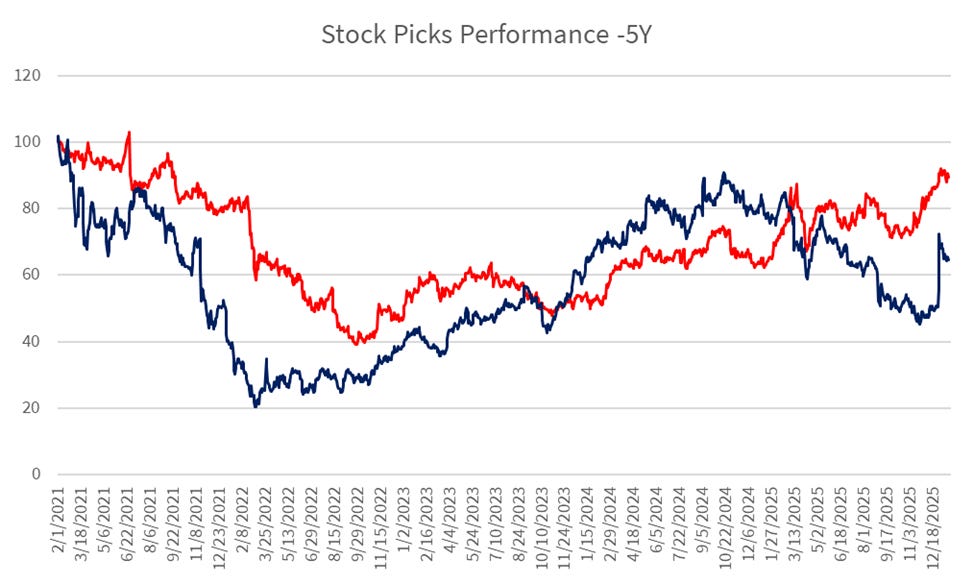

Stocks’ Performance

Source: AlphaSense

Both stocks have had weak share price performances for extended periods. One looks like it is starting to turn round and there has been a decent recovery, but the stock is still well below where it was 5 years ago, in spite of higher revenue and profitability. The other had been very weak and the bid speculation has boosted the price, but there is still 50% upside to its prior peak.

Premium subscribers can read on for the full story on both these interesting situations.

First a word from my sponsor:

Tracking Earnings Season Trends with AI

Earnings season delivers a data-driven view of companies, industries, and the broader economy. AlphaSense’s Deep Research and Generative Grid was used to aggregate recent earnings and conference call transcripts to show how companies in diverse industries are deploying AI across business functions.