TW3 - Why Accounting Works

…in the End

I normally try to write these articles well in advance, although sometimes I leave it until the Monday before publication. I try not to chase the news as I want to produce enduring content which will still be of interest in 12, 24 or even 36 months’ time – this is my 178th article on Substack and there may even be a book coming at some point.

But this week was so interesting that I decided to write this article before I head to a yoga class, in spite of fine weather in London on Saturday morning.

Last week

Monday – Eurofins crumbles as Muddy Waters launches a short campaign

Friday – Nike falls 20%

Friday – Bill Ackman prices Pershing USA at $50/share

Let me explain why these attracted my interest, but first, can I mention a webinar on accounting red flags I did for my sponsor, which I think many of you will enjoy.

After watching, you’ll know:

A short test that identifies red flags left by frauds

The best place to start looking for a manipulated balance sheet

How to “reality check” a company’s earnings in seven minutes or less

I think this is worth an hour of your time, let me know.

It really helps me if you sign up for these promotions, as my sponsor can see that their investment is delivering. Without sponsorship, the newsletter and podcast are loss-making , so please let’s give my sponsors some love…

Pershing Square USA IPO

Bill Ackman is a master marketer. He announced the price of his upcoming closed-end fund, Pershing Square USA, but revealed neither the number of shares nor the timing. I wrote about his move to sell 10% of his management company recently. The press are writing about the $50 offer price, which is meaningless – whether the stock price is $5, $50, or $500 makes little difference. But the excitement and hype surrounding this transaction is indicative of the later stages of a bull market.

I should also add that some of you got in touch to explain that Ackman’s intention is to invest in different stocks in this vehicle from his existing European closed-end fund. I had assumed that he would somehow try to equalise the two portfolios, an incredibly difficult challenge to be fair, in order to minimise potential conflicts of interest. The attraction of such a strategy was a view shared by a number of my serious professional contacts, but I can see the practical limitations and why a fresh start might be preferable.

I do wonder how the conflicts will be managed, however. Let’s say Bill or his team have another genius Covid-style 100-1 trade, to turn $27m into $26bn (probably an unlikely outcome). Where would he choose to deploy this capital? There are several options:

In a personal vehicle or one in which his partners co-invest. The argument could be that $27m is too small to spread across both funds. But this raises the risk of lawsuits from two sets of fund shareholders and from the shareholders of the asset manager (although he could use that as the investing vehicle). There is also an expectation that managers should not compete with their clients.

In the European vehicle – Bill is incentivised here by a performance fee so the firm would participate in the gain, further enhancing the value of the asset management company, which now has external shareholders. But shareholders in the quoted US fund might be upset at missing out, and there may be some lawyers among them.

In the US vehicle – this has the disadvantage that the gain will only accrue 2% management fees in later years and Bill and partners may own less stock than in the European vehicle. Meanwhile shareholders in both the European vehicle and the asset management company may be irate.

I am looking forward to watching these developments. Ackman is not charging fees in the US vehicle in the first year so he may take time to deploy the capital. Or perhaps his team of 8 analysts are so smart that they already know what they are going to buy with their $10bn $25bn, and they will perform out of the starting gate. Watch this space.

Forensic Accounting

Both Eurofins and Nike appear in my Forensic Accounting Course and have done so for several years. This is a course I mainly deliver in person or over Zoom to institutional clients. It has been incredibly popular and over 800 people have taken the course since inception. I was originally commissioned to build the course by Stewart Investors who were concerned that new joiners since 2009 had only seen markets go up.

To build it, I spent several weeks in the British Library, studying past frauds and looking for examples of accounting shenanigans. The course has 150-200 real life examples of companies cheating. The rationale was that after 10,000+ hours of practice, I can open a set of accounts and often can spot problems very quickly – the idea was to compress that knowledge and experience into a course of under a day.

It was never my intention to suggest that these were stock recommendations, and clients generally understood this. I was quite concerned when one manager of a $30bn fund walked out of the meeting room after just 90 minutes; he came back 10 minutes later with a printout of the portfolio and told me that he just wanted to check that he had a big enough short on a couple of the examples. More often, clients would disagree with my thesis and highlight that it was a company they had known for a long time and that they were comfortable with the position. And that was fine, as I was there to teach, not to offer recommendations.

This week, coincidentally, two of the stocks highlighted in the course fell sharply. On Friday, I was delivering a different course to a team of data scientists in New York. I have a couple of clients who have teams of data scientists - I help them become more familiar with how to analyse company accounts. Our last session is a practical case study where they choose an example and I do the fundamental analysis live, and they can study my process and reasoning. It’s quite fun, and quite challenging as I have to think on the spot.

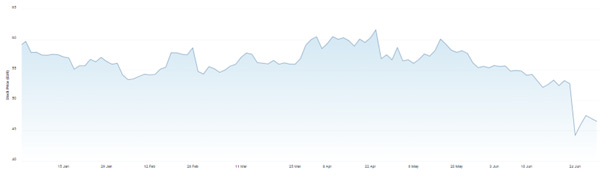

Nike

They picked Nike as the example, as it was down 20% on the day after guiding to a revenue decline in the new fiscal year. Nike had already fallen quite steadily this year, as you can see from the chart. We went through the statement, the consensus estimates, discussed the prospects for further warnings and tried to gauge the current valuation vs that risk.

Nike Stock Price YTD

Source: Alpha-Sense

I then explained why I had picked it as an accounting offender and why I wasn’t confident that the management were being as open as they should be with investors. My slides dated back to 2019, and one of the data scientists responded that all this forensic accounting is nonsense, you would have missed a massive run in Nike from 2019-2022. And I agreed with him, up to a point.

Nike Stock Price -5Y

Source: Alpha-Sense

The problem with the forensic accounting analysis is that while it can reveal that a company is massaging its earnings, it doesn’t tell you when that will be noticed by the stockmarket. And the fact that Nike stock is roughly back to the level when I highlighted its accounting shenanigans is a coincidence – it has taken a problem in the stock’s fundamentals to cause the share price to crack.

Nike Valuation Trends

Source: Alpha-Sense

This is why shorting is so difficult. You can be a brilliant analyst like John Hempton at Bronte Capital in Australia. He spotted that Wirecard was a fraud very early on and tipped off Dan McCrum at the FT; but it took 9 years for the fraud to unravel and John actually lost money on the short.

Where the forensic analysis works best in my view is in helping understand that a company you thought was a quality business isn’t as good as you thought – it’s growth isn’t quite as high as it looks; and when management resort to accounting trickery to support the valuation, you know that you should be thinking about an exit. In my view, accounting and valuation are joined at the hip and you cannot value a company if you don’t understand the quality of its accounting.

Eurofins

On Monday I met with a client to review a training programme I had given the whole team and to discuss what we learned and what we might do next year. This is a $1bn+ hedge fund which specialises in accounting shorts and the principal was in a good mood as he was short of Eurofins which had fallen 16% that day on the back of a short seller report from Muddy Waters.

Again, Eurofins was featured in my Forensic Accounting Course as a risky stock, for a couple of reasons. Its long term share chart is not dissimilar to Nike, funnily enough, it continued to do well for 2-3 years after I featured it, helped by Covid:

Eurofins Stock Price -5Y

Source: Alpha-Sense

But it had halved from the peak to the start of this year and it has been dismal this year:

Eurofins Stock Price YTD

Source: Alpha-Sense

Carson Block told me “There have been so many flags with this one for years”. The stock price was boosted by the pandemic and these situations often take considerable time to unravel. But you don’t get advance warning of the unravelling, and once the market loses trust in a situation, it can take a long time to restore confidence.

Eurofins Valuation Trends

Source: Alpha-Sense

In the case of Nike, the market isn’t worried about its accounting, at least not yet. And if it can resolve its revenue growth issues, it may be able to repair its valuation. In my experience, however, companies which have been resorting to accounting trickery to boost their growth and valuation often take considerable time to repair their fundamentals – because when the revenue growth slows, management see little point in flattering the accounting. Hence the earnings decline and the stock price fall are much larger than otherwise.

Premium subscribers can read on for a peek at the issues I identified. We shall run a cohort version of my Forensic Accounting Course for smaller funds over Zoom in October, an in person course in New York for 20 people from a range of different funds in November and naturally we are happy to deliver the course to any institutional client. Email me at info@behindthebalancesheet.com to learn more about any of these.

Note: The title of this article TW3 or TWTWTW is a reference to an old TV programme, “That was the week that was”