The $4.4 Trillion Question

Why the AI investment boom may require 10 million job losses simply to justify the investment

James Aitken

One of the most popular guests on the Behind the Balance Sheet podcast was macro strategist James Aitken, so I was delighted to welcome him back for a second appearance. Last time we took a tour of the world’s financial plumbing. This time we tackled some of the biggest themes facing investors today: AI, inflation, commodities, the dollar, market structure and the coming wave of mega-IPOs.

What makes James particularly interesting is that he works with some of the world’s largest and most sophisticated pools of capital. Rather than focusing on quarterly earnings or the latest headline, he spends his time thinking about the forces shaping markets years into the future.

One of his most thought-provoking observations was that investors may be asking the wrong question about AI. The question he hears most often is “when does the AI bubble burst?” His response is simple: bubbles rarely burst when everyone is worried about them bursting.

More importantly, he argues that investors underestimate how much infrastructure still needs to be built. It’s not just data centres. The world is shifting from decades of prioritising efficiency to an era focused on resilience, security and redundancy. AI data centres, electricity generation, defence spending and supply chains - the common theme is the future looks more capital-intensive which is potentially inflationary.

That naturally leads James to the “picks and shovels” of the AI boom. While many investors focus on Nvidia and the hyperscalers, he is increasingly interested in the less glamorous businesses that provide the physical foundations of the digital economy. We discussed commodities, power generation and companies such as Bloom Energy, which he uses as an example of how disruption often emerges in places investors are not watching. One of his key messages was that the physical economy has become remarkably under-owned by investors, yet it’s core to all these technological advances the market has been celebrating.

The other theme to note was his comments on a changing market structure. He believes investors should pay closer attention to supply and demand for equities. For years, corporate buybacks have steadily reduced the supply of listed shares. Now we are approaching the opposite dynamic, as I outlined a couple of weeks ago.

The AI hyperscalers are spending vast sums on infrastructure, not just slowing buybacks but creating issuance. Meanwhile, private-market giants such as SpaceX, and Anthropic and OpenAI (eventually?) to come, will bring new equity supply to public markets. James isn’t predicting disaster, but he does think the market’s ability to absorb this supply will be one of the most important investing stories to watch.

Perhaps my favourite insight came when James described the habits of the very best investors he works with. Faced with an endless stream of news, research reports and opinions, they create time to think. Rather than searching for another economist’s opinion, they pay close attention to what their highest-quality portfolio companies are telling them about the world. It sounds obvious, but in an industry obsessed with information, the edge may increasingly come from filtering noise rather than consuming more of it.

LVIC 26

I attended the London Value Investor Conference on Wednesday. It was a great event with an impressive lineup. Richard Oldfield introduced the conference with a summary of the performance of the last 3 years’ events:

Cumulative Performance %

This is a group which is worth listening to. The speakers this time were:

David Samra of Artisan Partners (a former podcast guest who manages a $50bn fund)

Rama Krishna, founder of ARGA IM, a $31bn value manager

Molly Pieroni, of famed Texas value manager Yacktman Asset Management

Sarah Ketterer, CEO of Causeway Capital, a $79bn west coast global boutique

Aileen Gan, CIO of Mondrian’s Global and International Equity Products

Brian McCormick who runs $1.5bn in global equities at Jupiter (he has done my Forensic Accounting Course, so of course he is really good)

Alex Roepers, founder of Atlantic IM, who has done 3x the S&P over 30+ years before fees

Dr David Walsh, Head of Investments at A$19bn quant shop RQI Investors

Gary Channon, founder and CIO of UK shop Phoenix, past podcast guest and frequent flier here

Guy Lakonishok, Partner at quant shop LSV ($100+bn AUM) who spoke about AI

Simon Adler, head of Schroders value team who pitched an interesting cheap Japanese stock

Duilio Ramallo, who runs an $11bn fund at $140bn Boston Partners, gave an outstanding presentation on AI which I run through below

Alexander Philipps, CIO of $8bn boutique Longview Partners with an interesting US large cap

Sam Ziff, CIO of Oldfield Partners, discussed one stock I already own and one I sold (higher up)

Ben Watsa of Marval Capital pitched a fascinating Asian name I didn’t know which is down 50%

Rich Pzena was interviewed by my friend John Heins and discussed a few stocks, including one I own (thanks to one of his colleagues) which has doubled too quickly and I haven’t yet added.

AI – Will it Make Money?

Diulio Ramallo of Boston Partners gave an excellent presentation on the investments going into AI and why he believes they won’t generate an adequate return. I had done some of this analysis but didn’t have the technical knowledge or the access to complete it, so I wanted to share his presentation with you.

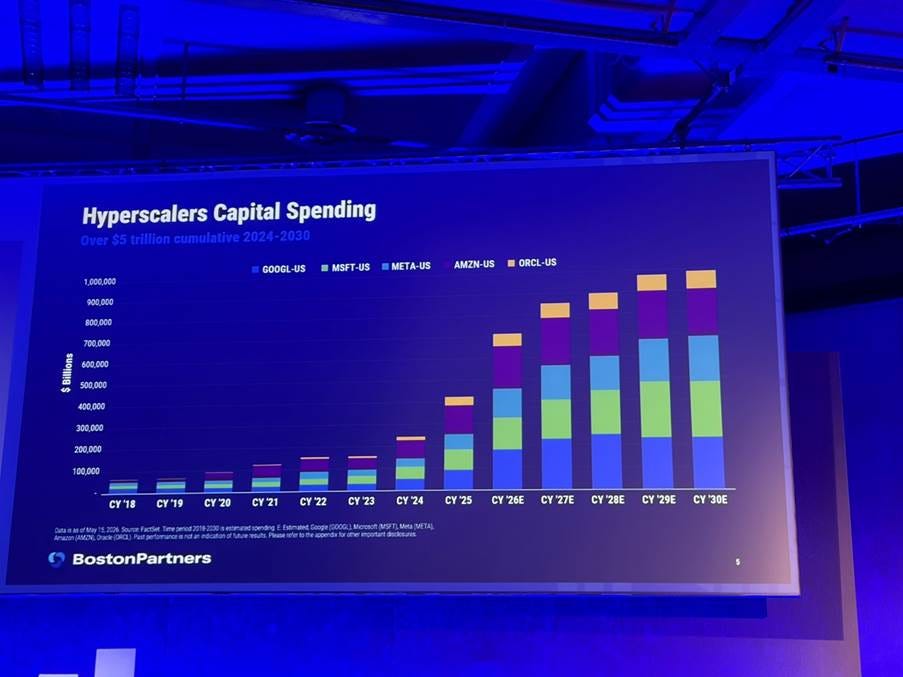

He first analysed the capex going in, a feature we all are familiar with – here is his slide on the hyperscalers’ capex which he estimates will hit $1tn in 2030 (and will reach nearly half the S&P500 total by 2028):

Hyperscalers Capex

Source: Boston Partners

This relative spend is more than unusual, it has no precedent:

Top Spenders Through the Decades

Source: Boston Partners

The primary issue is that the costs of building a data centre are huge. Here are his estimates of the cost of the racks for a 1GW data centre, using NVL72 GB300 chips. Sources include broker research.

Chip cost for 1GW Data Centre

Source: Boston Partners

Here are his estimates for total cost, with the physical infrastructure including the site cost, shell, power and advanced liquid cooling.

Total Cost 1GW Data Centre

Source: Boston Partners

He then calculated the depreciation charges:

Data Centre Depreciation Costs

Source: Boston Partners

I revised this slightly in my calculations to give the building a 50 year life and the ancillaries and cooling systems etc a 10 year life and I came to $7.9bn - $8bn is good enough.

He then calculated the operating costs as electricity $1.3bn and maintenance and other at $1.2bn – to give $2.5bn in total. His interest line assumed a 50:50 equity:debt capital structure and a 7% interest rate – that seemed low to me, but obviously it will be cheaper for Microsoft than Oracle and it depends on the structure. But that’s $1.75bn. That takes total costs, including depreciation, to $12.3bn.

Up to this point, Ramallo had demonstrated the extraordinary scale of AI investment and given us a reasonable estimate of what it costs to build and operate a 1GW AI data centre.

The obvious question is whether those economics ever produce an acceptable return?

Using Ramallo’s assumptions, I built my own model to answer exactly that question. The results have important implications not just for the hyperscalers, but for Nvidia, OpenAI, Anthropic and almost every investor trying to profit from AI.

The conclusion surprised me. Even assuming the data centres earn what I would regard as only a modest return, today’s AI infrastructure spending would ultimately need to replace more than 10 million knowledge workers simply to justify the investment.

After the paywall, I walk through the model step by step, explain why the economics resemble previous infrastructure booms, discuss where the profits are most likely to accrue across the AI value chain, and finish with my detailed notes from the conference, including 19 investment ideas from some of the world’s leading investors, several of which I already own or am researching further.

Before that, my podcast sponsor AlphaSense has come up with a special offer for my readers:

How many positions have you passed on simply because there wasn’t enough time to go deep? AlphaSense AI-Led Expert Calls run expert interviews on your behalf, so coverage gaps become a thing of the past.

From Tegus by AlphaSense