That Was the Week That Was: Hype, Hope & Hidden Value

Tech extravagance, a red flag hiding in plain sight, + 4 cheap quality stocks from a top fund

TW3

It has been something of an absurd week, so I wanted to share a few things. TW3 is a reference to an old early 1960s TV show, That Was The Week That Was, fronted by David Frost with a cast and writers which included some of the greats of British comedy (John Cleese, Peter Cook, Richard Ingrams, Frank Muir, and many more.

OpenAI/Sir Jony Ive

Ive, former collaborator of Steve Jobs, is a genius designer. He sold the remaining 77% in his hardware start-up Io - not his design studio, Love From – to 23% holder, Open AI. The valuation of $6.4bn is $116m per employee (still cheaper than WhatsApp). This could be

one of those ridiculous transaction at the top of the hype cycle moments, or

perhaps they have a substitute for the iPhone (Apple fell 2% on the day, but Samsung was only down 0.4%, so no idea if this was a contributing factor), or

AI has such huge potential that $5bn here or there is just a rounding error.

In tech, what seems daft at the time (Facebook paying $1bn for Instagram when it had 13 employees and was 18 months old) can prove to have been a genius move in retrospect. This may be one of those.

On AI, Marc Andreesen, who I think is worth listening to, recently suggested that AI will drive the cost of production down, not just of digital products but physical goods, and will create a deflationary spiral – you know the Japanese phenomenon of why buy today when it will be cheaper tomorrow. And Marc Benioff of Salesforce and others say we are just st the beginning.

Tesla CFO Pay

My friend Chris Bloomstran tweeted about the Tesla CFO’s $139m pay package. Vaibhav Taneja was only promoted to the position in August, 2023. I don’t know what to say about such ridiculous levels of pay – much smaller bonuses are normally awarded for years of superior performance. The Wall Street Journal’s list of top 10 CFO pay included two frauds, Nikola and Valeant, and a number of companies whose earnings have been heavily manipulated (allegedly). The #2 award, to the Nikola CFO, was $86m.

Tesla CFO Package

Base salary is $400k

Stock options: $113m, granted October 2024. Shares are $335, up 34% from c.$250 level at time of award.

Restricted stock units: $26m

Vaibhav Taneja has been Chief Financial Officer since August 2023. Prior to that, he was Tesla’s Chief Accounting Officer from March, 2019, Corporate Controller from May 2018, and Assistant Corporate Controller between February 2017 and May 2018. Mr. Taneja served in various finance and accounting roles at SolarCity from March 2016.

Taneja has sold several thousand shares of Tesla this year and now has 112,950 common shares worth c.$38m, with 26,950 shares held directly. The 2024 proxy statement indicated ownership of 1,063,554 shares and options at March 31, 2024, before the latest award.

Obviously we want our managers to have skin in the game and to prosper with company success. But I have a bit of a problem with CFOs getting inflated 3 year RSUs or bonuses especially where they are contingent on eps growth and similar parameters. If you give someone a huge incentive to cheat with the numbers, you will get the numbers you are looking for.

And don’t get me started on someone who has only been in the position for under 2 years. I cannot find the criteria for Tesla’s stock option awards, although they apparently are tied to revenue and profit milestones. They appear to be granted at the then share price and represent stock appreciation which would be a comfort. But this award seems ridiculous.

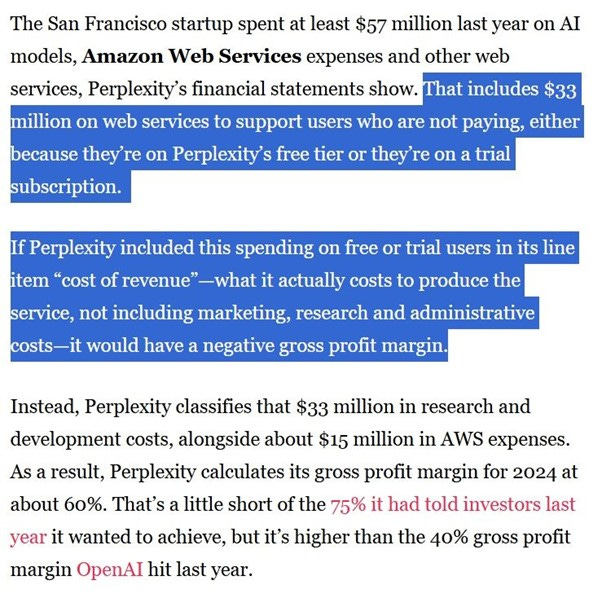

Perplexity Manipulation

The Information (a tech publication) wrote that Perplexity spent $33M on AWS last year for users on its free tier or trials. They booked this as R&D. Some more aggressive CFOs like to inflate R&D as investors assume an element of R&D is investment - there is an implicit return expectation.

The correct treatment of this item would be either cost of goods sold or selling expenses. It’s part of the cost of delivering the product, so I would think that would deliver a better picture of underlying gross profit.

One could also argue that it’s part of customer acquisition cost and therefore, treating it as a promotional expense under selling expenses or SG&A would also be correct. Perplexity apparently wanted to exclude it from COGS as otherwise gross margins would be negative. I cannot imagine its gross margin would be very high and I am not sure investors would be bothered. But it’s absolutely not R&D, a point the article below missed.

I think this is an interesting example of the type of shenanigans which are being conducted wholesale in the VC space (and in private equity, but they tend to use auditors to check the numbers as part of due diligence, and then use that report as part of the price negotiations). Interestingly, I had a call with a VC head two weeks ago who wanted me to design a training programme for his juniors. I am surprised that I don’t get more such inquiries, but then perhaps VCs expect their investees to go bust.

CNBC reports that Perplexity’s annual recurring revenue is under $100m, and given the growth, its last reported revenues would be significantly smaller. Its current round is reported to be at an $18bn valuation, twice the previous level.

Source: The Information (via LinkedIN)

Buffett

The Omaha Herald reported that Mr Buffett has decided he won’t take the stage at next year’s meeting. He will attend, but will sit with the other directors.

I was surprised as I thought Mr Buffett enjoyed the limelight, felt an obligation to his fans and wanted to support the local economy (the weekend is worth over $100m to Omaha each year).

Woodstock will continue, but it won’t be quite the same.

Markets

Highly respected strategist Chris Wood has publicly called the top in the U.S. share of global markets and sees a weaker dollar as being an ongoing driver of this trend. I agree and the global ex-US market chart is supportive.

Meanwhile, the 30 year Treasury has hit 5%. Higher rates are unhelpful for stockmarkets. I think the setup for physical commodities is positive, but I am less confident on stocks.

LVIC 25

Last week I attended the London Value Investor Conference which had a mix of value and quality ideas from a dozen professional investor presenters who paid to pitch their best ideas to an audience which included the two largest allocators in the world.

Next week, I discuss the two fireside chats, with former podcast guest Sebastian Lyon and financier and former White House Communications Director, Anthony Scaramucci.

This week, premium subscribers get 4 ideas from a $50bn California-based top fund manager whose top pick last year was up 85% and this year again has the best performance, with one stock up 10% in less than a week. Two stocks pitched last year and repeated are down 8% and 17% and the fourth is up 3%. This is an interesting cocktail that you don’t want to miss.

I love this quote from the 2025 Berkshire annual meeting which I highlighted last week:

“I spend more time looking at balance sheets than I do income statements…. I like to look at balance sheets over an 8 or 10 year period before I even look at the income account…There is a lot to be learned and you learn more from the balance sheets than most people would give them credit for.”

Warren Buffett

I included an offer last week and some people had difficulty – there was a technical glitch with the coupon code. I therefore decided to extend the offer by a week. My course How to Read a Balance Sheet (and the Other Statements) covers the entire financial statements plus modules on financial ratios and accounting shenanigans, but the name was founded on the same principles that Mr Buffett highlighted. It’s normally £399 or $499 but if you use the code PREMIUM24 for the sterling or PREMIUMM24 for the $ version, you will get 30% off. Hurry – it ends this week.

Simply hit “Enrol” and choose £ or $.