4 Forms of Tail Risk Protection

Including one I recently added to my personal portfolio

Last week I covered the Ruffer keynote from the Moneyweek Conference 2023 in London and I am following up with some observations from the other excellent keynote from James Montier of GMO. Montier is always a thoughtful and interesting presenter and this time was no exception. First a word from our sponsor:

Expert calls just got easier.

Say goodbye to traditional expert networks with Stream by AlphaSense. Stream enables you to access high-quality expert insights, in less time and at lower cost. With proprietary search technology and a library of more than 26,000 expert call transcripts, Stream provides the tools to help you make smarter decisions faster. Sign up today.

Montier’s presentation assessed the risks posed by present market conditions. He referenced a book by Richard Vague (The Next Economic Disaster: Why It's Coming and How to Avoid It) which argues that it is the rapid expansion of private debt that constrains growth and sparks economic calamities like the GFC, the 1929 crash and others. Vague’s algorithm suggests that

1) Private sector debt of over 150%, together with

2) A five year rate of growth in private sector debt of over 18%

multiply risks to the economy.

I am always a little suspicious that things are this simple and the next crisis is usually somewhat different, but the basic argument makes sense: Government debt can be printed away or subdued by financial repression and it’s private sector debt which creates the real risks to the economy.

Montier pointed out that the US is at danger levels of private sector debt:

US Private Sector Debt Warning Signal

Source: GMO

He also highlighted that this level is an issue in the UK, France, Spain and Australia. But the rate of growth could be less of an issue as it’s below Vague’s level:

US Growth in Private Sector Debt below Critical Level

Source: GMO

But Montier argued that it’s the level of private sector credit that is probably the more critical factor and I would agree. Instead of the level of growth being the trigger, it could be interest rates. The Fed has raised rates aggressively – the interest cost will rise in a similar way to a significant increase in the amount of credit.

Moreover, there are additional factors which we should be concerned about:

1 the risk of recession

2 the level and valuation of the market

3 the concentration of that debt by sector (my addition)

Leading indicators are suggesting a high risk in the US economy:

Leading Indicators are Gloomy

Source: GMO

Montier was sceptical about suggestions of a soft landing – he thinks they are unusual. This is probably particularly true of credit stressed downturns – think of the Tequila crisis in the early 1980s or the Asian crisis in the mid-1990s.

Meanwhile, market valuations are high in the US as evidenced by this chart from Schroders:

US Stockmarket is not Cheap

Source: Schroders

And profits are also high which could prove a significant problem:

US Economic Margins are Near Peak Levels

Source: GMO

The reason this creates vulnerability is two-fold:

1 inflation: it’s likely that in an era of higher inflation, margins will trend down as companies experience cost pressures and many struggle to pass these on to customers.

2 the starting level of margin is extremely high by long term historical standards. Montier has been writing about this since 2011. The fact that he has been early does not mean he will be wrong.

Having established that there are serious risks, Montier then discussed the best way to protect portfolios and highlighted three routes:

1 Holding cash

2 Using options

3 Using strategies with a negative correlation to tail risk

Holding Cash

With interest rates of c.5%, it’s perfectly sensible to hold bonds or cash. Paying subscribers can read below what I am doing in this respect. In contrast to recent years, you are now being paid to wait.

Using Options

Montier pointed out the attraction of CDS strategies in the runup to the GFC but option protection is rarely cheap and requires a level of sophistication which is above my pay grade. The problem is that the premium to protect against tail risks is usually very expensive.

Negative Correlation Strategies

Montier talked about three main strategies:

1 long volatility

2 quality minus junk

3 value minus growth

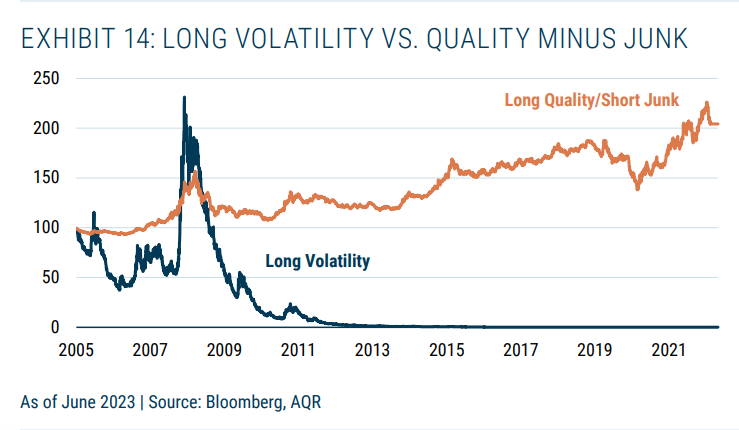

Buying volatility contracts give you a protection against a market crash if credit blows up the US economy. But it’s too expensive. Montier showed that a strategy of quality minus junk has in the past had a much better return:

Longer Term Quality Minus Junk Beats Long Volatility

Source: GMO

And even over the pandemic, this strategy fared better:

Short Term Quality Minus Junk Beats Long Volatility

Source: GMO

The problem here is two-fold. It’s quite difficult to execute a quality minus junk strategy if you are a retail or a long-only investor. More important, quality is very expensive:

Quality is Expensive today

Source: GMO

This is a really important point. Not only are markets highly priced (Montier prefers emerging markets on a CAPE or cyclically adjusted P/E of 11x vs the US market on a CAPE of 30x), but quality is priced more highly than at any point since the 1980s. Had the chart gone further back, quality was probably more highly priced in 1969 in the era of the Nifty 50, but we know how that ended (disastrously!).

The quality/compounding fraternity may escape from the next decade unscathed but onE important reason why Terry Smith has performed so well may be that his portfolio and quality stocks more generally have enjoyed a fabulous rerating. It’s unlikely in my view that this rerating is repeatable from current levels.

With quality at a premium valuation, Montier highlighted his preference for value minus growth. The table shows that this hasn’t been as effective as tail risk protection historically, but given the valuation of quality, a value vs growth strategy may fare better going forward:

Tail Risk Strategies’ Historical Performance

Source: GMO

The table shows that quality minus junk has been the most effective strategy in the past but it seems less likely to be the best protection for the next crisis.

Montier went on to discuss the level of portfolio protection you should take. Premium subscribers can read on for this discussion and to hear about a potentially cheaper form of downside protection that I’ve recently added to my personal portfolio. Of course, this isn’t investment advice.

I should conclude this section by mentioning the sectoral exposure I touched on earlier. To be clear, this was not part of Montier’s talk but is significant in my view. The private equity owned corporate sector today is at a record proportion of the US economy – proper data is hard to find but this conclusion is clear. And these companies tend to be highly indebted.

If there is a major credit event, as Montier suggested is likely at some point, timing uncertain, then almost inevitably the epicentre seems likely to be in private assets. This has significant potential knock-on impacts as the sector is geared not only at the level of the underlying investments but increasingly at the portfolio level through NAV loans which have been attracting more attention lately.

Debt piled upon debt – what could go wrong? More on this in a future Substack.