Legends, Leaders, and Sohn London: Exclusive Insights & Investment Pitches

Carson Block and 13 other must-know ideas from Sohn London, Anthony Bolton on investing and the FTSE 100 Boardroom view of the UK

Sohn London is one of my favourite conferences of the year. It offers a chance to catch up with old friends, make some new ones and hear from some of the biggest hitters in the hedge fund world. This year, I could not stay too long at the drinks afterwards as I had another drinks party - it’s ironic to have two fabulous events on the same night when you lead a quiet life.

Before getting into it, a word from my sponsor, AlphaSense:

Don’t Miss This Rare Opportunity: Live Discussion with Patrick O’Shaughnessy & Industry Experts

I’ve been following Patrick’s insightful commentary on how he's leveraging AI and I must admit, his approach is far ahead of mine. That’s why I’m excited to invite you to a rare, live-streamed panel discussion hosted by Patrick on AI’s Impact on Investing.

He’ll be joined by Divya Narendra, CEO of SumZero and co-founder of ConnectU (the predecessor to Facebook, as seen in The Social Network), and Chris Ackerson, VP of Product at AlphaSense. Together, these industry leaders will explore AI’s transformative role in the investment world, covering the latest trends from FAANG to FinTech and the profound effects on financial institutions.

It’s Black Friday next week and each year I make a one time discount offer on an online course to my lovely subscribers. Get 20% off How to Read a Balance Sheet, which has everything you need to know to understand and analyse financial statements. Use the code BF24.

This offer has a limited availability until December 5.

It was a busy week last week and apart from the Sohn conference, I flew to Edinburgh to interview Anthony Bolton (listen to the podcast) and went to the Sunday Times Business Christmas party. This is attended by all the serious business chiefs and is a great way to take the pulse of UK plc.

UK State of the Nation

Britain’s leaders are gloomy. One notable private equity entrepreneur, a household name in the UK and a centimillionaire, said he doesn’t feel like investing here, and that’s the first time he has felt like that in a 30+ year career. Andy Brough, a notable UK fund manager, known for his forthright views, joked that he was in charge of liquidating the UK stock market – he couldn’t count how many of his investees were bid for this year. One well-known business figures told me he thought the Labour Government were clowns, another said “clueless”.

The rise in employer National Insurance (a tax on employing people – I am not making this up) has hit hard. On the plane up to Edinburgh, the lady next to me (middle seat free in row 13) is in charge of HR at a care home operator, owned by private equity, naturally. She looks after 5,000 staff and the change in NI and minimum wage means a £3m increase in costs on a £180m revenue base. I thought the hike would simply be passed on, but local authorities have restricted budgets.

Back at the party, the main speaker was new Conservative Party leader, Kemi Badenoch, who made a really amusing speech and grabbed the audience’s attention. Last year, they were all for Rachel Reeves, but business seems ready to forgive and forget. She pointed out that the new Cabinet lacked business experience and highlighted the new addition to the Shadow Cabinet, former Sky CFO and COO, Andrew Griffith (now Shadow Secretary of State for Business and Trade) who she claimed had more industry experience than the whole Cabinet. She received a warm welcome.

Anthony Bolton Podcast

I had a high spot and a low spot last week with the podcast. It was amazing to have the opportunity to spend time with Anthony Bolton, one of my investing heroes. But I could not help reflecting on Peter Cowley, the angel investor whom I interviewed earlier this year. He was dying, but was still cheerful and upbeat when I met him in the podcast studio; every day for weeks after, I would think of him when I had some minor setback or irritation and realise how lucky I was. Peter passed away peacefully last week – I am grateful to have met him and glad his life ended as he had wished. I know I will continue to think of him. My condolences to his wife Lies (whom I met at his book launch) and family. Peter supported the Papyrus suicide prevention charity.

It was an enormous privilege to interview Anthony Bolton, the legendary fund manager, at the Library of Mistakes in Edinburgh in front of a star-studded audience. It was my first live podcast interview and I would have been nervous interviewing Bolton in the studio or interviewing anyone live in front of any audience. It all went well, and Anthony is a true gentleman. I don’t know how he managed to deliver nearly 20% pa for 28 years AND be such a nice person. Here is what one of his former colleagues wrote to me, on hearing that I was doing the interview:

“I noticed that you had Anthony coming onto the podcast in a couple of weeks time. I was incredibly fortunate to have worked closely with Anthony when I joined Fidelity and then to have had him as a mentor when I began managing portfolios. He has an exceptional mind, a natural, insatiable curiosity for stocks and is quite simply the bravest fund manager that I’ve ever met. More than that he is a wonderfully kind, courteous and generous individual and I can’t thank him enough for the advice and wisdom that he shared with the investment team.”

Do listen to the podcast, but one important takeaway is that Anthony thinks the US market is near the top

We had dinner afterwards at Walter Scott, and (unusually) I was one of the younger men round the table. Such a lot of wisdom, not just from Anthony but also from Max Ward – he retired last year after 50 years as a fund manager, starting at Baillie Gifford - and Angus Tulloch, the Emerging Markets guru, who retired in 2017, after 29 years as a fund manager.

Tulloch told me that he always underperformed in bull markets but made it back in down markets. He told his team to do as he said, not as he did - because he liked to have the odd flyer on something exciting, but never more than a 1% bet; he reckoned he made a net zero on these bets, but they were good fun.

It strikes me that the industry is much more professional these days but much of the fun has been lost. Which I think is a shame.

Sohn London Conference

I have written this up before and it’s always a popular post. This year was especially good. There were 3 great short ideas and 11 longs, although one of those could have been a short – a governance-focused fund trying to take on a maverick billionaire. More on that next week.

Speakers included two former partners of Chris Hohn’s TCI, long only funds, long-short funds, a private equity type fund, and a macro fund with a sovereign bond idea. One quality growth stock was aired here before. I started to dismiss it, until I understood the presenter’s new angle – he later told me in private that his fund was up 83%, year to date. I liked that optimism – there’s still another few weeks to play for.

The speakers were:

William de Gale, Bluebox AM

James Hanbury, Lancaster IM

Anne-Sophie D’Andlau, CIAM

Liad Mediar, Gatemore CM

Edgar Allen, High Ground

Stephen Shields, North Rock Capital

Mikhail Zverev Amati Global Investors

Thiago Mordehachvili, Granular Capital

Diego Megia, Taula Capital

Oscar Hattink, BlueDrive Global Investors

David Semeza, Islander Capital Partners

Ali Benzakour, Envestra Capital

Malte Heininger White Creek Capital

Carson Block, Muddy Waters Capital

I shall share the Muddy Waters pitch here, as it’s public, and premium subscribers can read on for the full list of ideas and a brief takeaway on each. I shall cover the ideas in detail in the next few weeks, and it might just be worth thinking about upgrading to premium. Surely you can make that back x10 or x100 pretty easily (not to mention the extra course discounts).

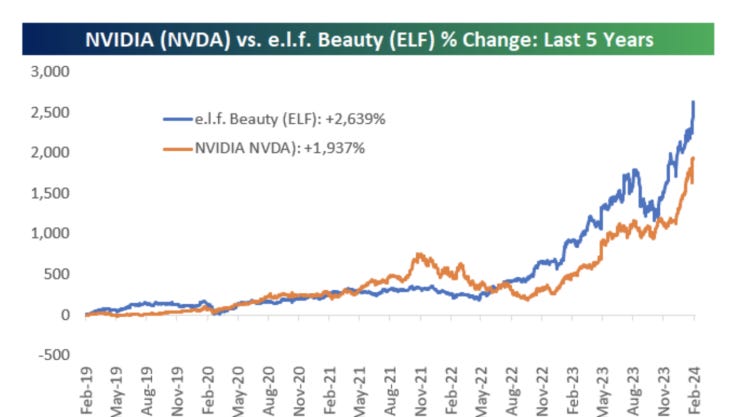

ELF Beauty

Carson explained that ELF Beauty has been a go-go stock, at one point ahead of Nvidia. They believe that numbers have been inflated and had an intriguing chart showing that sales which formerly tracked import volumes had suddenly diverged:

Elf Sales vs Import Volumes

Source: Muddy Waters Research

The thesis is that sales can only track imports and if the imports have collapsed, sales should have too – instead, sales, an important metric for management compensation, have continued to increase, which suggests that revenue growth might have been exaggerated.

Muddy Waters claims that revenue over the last three quarters has been overstated, possibly by as much as $135m or even $190m. From their report, “a recent change to its sourcing practices was responsible for the sudden appearance of an additional $36.9 million of inventory. ELF claimed that it had just begun taking ownership of product on the China side, whereas previously its practice had been to take possession only upon delivery to its Ontario, California warehouse.”

ELF added $36.9m of inventory in transit last quarter and Muddy Waters (MW) believe that there has been no change in practice and the inventory build is a result of falling sales.

The presentation focused on how to prove that sales had been inflated, first highlighting that ELF’s imports are a good way of tracking sales, as 80% of products are sourced from China.

Hence the comparison of the independent import data vs sales. Here is their chart of imports, this time vs inventory:

Source: Muddy Waters Research

Here is their estimate of import volumes, with management comments on inventory levels:

Source: Muddy Waters Research

The company increased guidance on its Q2 24 call and the stock was beating Nvidia by February, 2024.

Source: Muddy Waters Research

MW see Q2 FY 24 as a turning point – inventory was up $49.2m with all but $10m of that attributed to the change in sourcing. MW have verified with 3 of ELF’s 4 main suppliers that there has been no change in sourcing practice with goods always purchased FOB Shanghai or Ningbo – ie title was acquired in China.

I really admire the depth of Muddy Waters’ work – they don’t rest here. They then ask if perhaps the import data is flawed and used two different import data sources and then used a third source, a risk assessment platform, to cross check. They accept that ELF could have used a consignee, but as this would add expense, it’s unlikely.

The import data is by weight while the inventory is obviously a $ value. They then needed to establish that there was a consistent relationship between weight and value. The table shows their calculations of value per kg, with the spike supportive of their thesis:

Source: Muddy Waters Research

They cross-checked by referencing Chinese suppliers’ reports and accounts and estimating values per kg which supported the $20-ish per kg. As did an independent data service. They also purchased a basket of products and calculated the value per kg and estimated the average cost:

Source: Muddy Waters Research

A third corroboration was a quote from an ELF supplier which supported the lower cost per kg. They then reconciled the inventory data from Q3 FY 24 using the upper and lower costs per kg to identify the range of potential inventory overstatement which they put at $98-133m.

Source: Muddy Waters Research

MW then convert that using the group’s gross margin to a estimate of $138-188m revenue overstatement vs $1bn of revenues last year.

Naturally, the company has denied the allegations but neither the report nor the rebuttal have had as much impact as they sometimes do in these types of short seller situations - the shares are back where they were before Wednesday’s publication of the report.

ELF Beauty Recent Stock Price

Source: Google

And this is a seriously volatile stock:

Source: AlphaSense

The short seller attack barely registers!

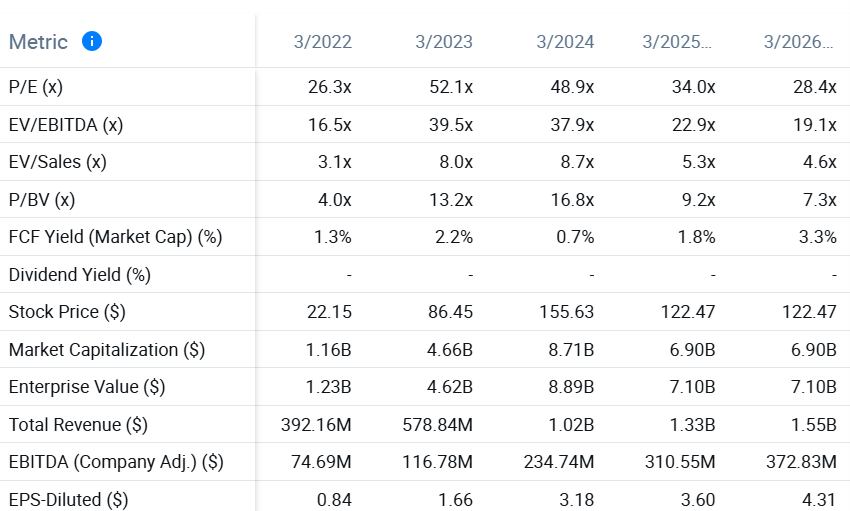

ELF Beauty Valuation

Source: AlphaSense

But if this company stops growing, its valuation will take a major hit.

Sales growth is 60% of management’s bonus incentive with adjusted EBITDA 40% and a further market share gain kicker on top.

And directors have been selling and at an increased pace since June ’23 when the inventory change was reported. Until then, the CEO had been selling at a rate of $4.3m per month and from 7/23 to 9/24 that pace increased to $7.5m/month. The CFO’s pace has picked up from $0.3m to $1.1m/mth.

This for me is an important tell – why would directors be selling stock in a company that was doing fantastically well?

I am a great admirer of Muddy Waters’ work and Carson and his partner Freddy Brick have become friends and great supporters of Behind the Balance Sheet. This was from an initial interview I gave to Zeroes TV during Covid. I did another looking at Greensill when it imploded. Their channel is good fun and worth checking out.

Premium subscribers can read on for a brief rundown of the other conference ideas which I shall write up in more detail in subsequent weeks.