Outlooks Galore

What the world’s biggest investors are expecting this year (Part One)

One of my most popular articles last year was a round-up of the investment banks’ forecasts for 2023. I thought I’d do the same again this year. Not only because you seemed to like it, but because some of this year’s outlooks are a lot more interesting. First, though, I’d like to clean up a silly mistake from last week’s post.

A Silly Mistake

Last week, I mentioned that our next Forensic Analysis Bootcamp will kick off on February 26, and that early sign-ups from my Substack readership can use a special promo code to save. Stupidly, I forgot to link to the course page.

The promo code for free readers is “EARLY” and there’s a bigger saving for my paid readers. If you can’t be bothered retrieving the promo code from the paid section of last week’s edition, reply to this email and I’ll hook you up.

This will be the third edition of the training. In addition to the core lectures, Cohort 2 received three bonus sessions: one to cover issues on valuation they had trouble with; a presentation from famous financial historian and author Russell Napier; and a discussion with investor and author Pulak Prasad!

Anyway, back to the 2024 outlooks…

What Are The Big Investors Expecting?

Last year, most of the outlooks I looked at were similar, reflecting fears of an imminent recession. Of course, they were almost universally wrong, as they probably are most years.

I say “probably” because when I was a professional investor, I paid no attention to any of these publications. This may mean you don’t want to read on, but there are always some interesting snippets in the banks’ work.

Blackstone

Regular readers will recall my farewell to Byron Wien, who penned his annual Ten Surprises letter for 38 years. Blackstone will be producing something different this year, but they wrote a piece about how the 10 Surprises for 2023 turned out.

They were right that the Fed wouldn’t pivot; were wrong in expecting a recession (as did almost every commentator); they correctly expected a recovery in markets; were bullish on European and Japanese assets (half right); were wrong to be bullish on commodities; and they bet that Elon Musk would turn Twitter around – on that they are certainly early and likely wrong.

It's refreshing to see a financial institution prepared to review its predictions in this way, but sadly rare. Spoiler: The ones I cover below might not be as accurate.

Blackrock

“The economy is normalizing from the pandemic and being shaped by structural drivers: shrinking workforces, geopolitical fragmentation and the low carbon transition. Seemingly strong U.S. growth actually reflects an economy that’s still climbing out of a deep hole created by the pandemic shock –and tracking a weak growth path.

Our bottom line for 2024: Investors need to take a more active approach to their portfolios. “

“A more volatile macroeconomic regime, alongside relatively high rates, may mean investors need to demand greater compensation for taking on equity risk.” They like AI, medical innovation and reshoring themes.

“Climate resilience is emerging as a new investment theme within the low carbon transition……. increased demand for solutions that help economies prepare for, adapt to and withstand climate hazards …. We see geopolitical fragmentation and economic competition driving a surge of investment in strategic sectors like tech, energy and defense.”

Barclays Private Bank

“The most anticipated recession in history is still nowhere to be seen. Simply because it didn’t happen in 2023, many investors are now expecting it in 2024. While each day passing brings us closer to the next economic contraction, we continue to believe that the whole “recession debate” is misplaced.”

“What we do expect is a world where economic growth trends lower, sometimes flirting with contraction. With that, we also expect inflationary pressures to recede, albeit gradually from here. With main central banks having been extremely aggressive in their pursuit of higher interest rates, we would expect them to change tack as the year progresses (given expectations of falling inflation). However, investors should be careful what they wish for: monetary policy may not turn accommodative unless the outlook meaningfully deteriorates.”

“Cash is now a comforting and arguably rewarding alternative. 2024 could be about extending (fixed income) duration to capture more than just coupons until maturity. Similarly, equity investors would need to tweak their allocation to favour sectors and regions that can respond well when growth slows and rates start falling.”

BNP Paribas

When I wrote last year’s article, I said “BNP are an outlier in their negativism”. This year’s report is titled “Stepping into a New Reality”. Highlights are:

“In 2024, the cash that drove economic activity in 2023 will start running low. In the US, excess savings will soon be spent, and business investment will wane. Europe is more vulnerable to recession risk and will face stagflation, while China struggles to resolve its property crisis. Tighter financial conditions will weigh on economic growth and corporate profits.”

They “favour government bonds over equities, anticipating lower bond yields as central banks cut rates to support growth, and lower equity prices as expected earnings fail to materialise.”

They like AI, disruptive tech, private infrastructure debt and China equities. Everyone likes AI, as you will see…

Cambridge Associates

“The cyclical backdrop will remain weak in 2024. The consensus expectation is for the global economy to grow 2.7%, which is slightly less than growth is anticipated to be in 2023 and below its post-2000 average of 3.5%. Risks are skewed to either matching the consensus expectation or missing it lower.

Three major drivers inform these views. First, credit growth in key markets is likely to remain subdued, given high interest rates and the increase in bank underwriting standards. Second, consumer spending growth is likely to either slow (United States) or remain slow (euro area and United Kingdom), given the depletion of any excess savings that accrued during the pandemic and weakness in consumer confidence. Third, numerous challenges, such as the war in Ukraine, the Israel-Hamas war, and China’s real estate crisis, will continue to weigh on sentiment and have the unfortunate potential to escalate.

We expect global equity performance will be below its long-term median level, but we believe investors should hold equity allocations …Within equities, we see opportunities in developed value, developed small caps, and China. We doubt European and emerging markets ex China equities will outperform.”

Within credit, they like “structured credits, particularly high-quality collateralized loan obligation debt, and we expect high-yield bonds will outperform leveraged loans. But we remain neutral on high yield because spreads are compressed”.

Citi Private Wealth

“Our analysis suggests that the global economy is healing and poised for further recovery.

Inflation is coming down. Wage growth is moderating, even in services.

Employment growth is slowing.

The US economy is more resilient than many expected.

Some US industries suffered a “rolling recession” in 2023. These sector contractions will roll out in 2024. Though the new year will initially see a slowdown in growth, there will be no broad-based economic collapse.

For many sectors and markets, equity valuations are more reasonable than investors believe.

Corporate profits are rebounding and are likely to hit an all-time high in 2025.

High short-term interest rates today are unlikely to be available tomorrow. The same is true for longer-term rates. Investors should not assume that they will be able to maintain rates as they roll over short-term Treasurys and bonds.

As rate pressures recede, the US dollar is likely to decline.

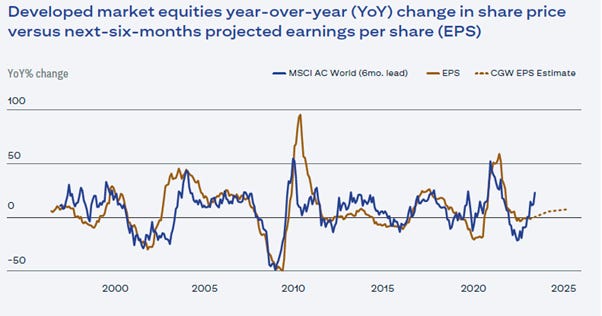

We expect global economic growth to strengthen in 2025. This should become apparent to investors as earnings estimates for 2025 rise. We expect a 12% increase in earnings per share (EPS) over the next two years.”

Equities to Benefit from Earnings Growth

Source: Citi Private Wealth

They also see value in growth small caps and mid-caps in the US:

Forward P/E of Growth Stocks by Size Band

Source: Citi Private Wealth

“In the past five years, the profitable SMID firms of the S&P 400 and 600 growth indices have averaged annual EPS growth of 11%. That’s even above the 9% pace of the large cap S&P 500 growth index. Yet, the SMID growth shares trade cheaper, for an unusually deep discount of 39% on current-year estimates compared to the valuation for the large cap segment. In fact, they trade 29% below their own 25-year history based on trailing price-to-earnings (P/E) ratio.

Deutsche Bank

This report is titled “top 10 themes for 2024”. I won’t go into all of them, but I thought this was quite an interesting report (link at end for premium subscribers).

“The big focus of 2024 will be the slew of elections around the world. We expect some volatility around these, particularly if markets become nervous about fiscal spending promises.

For corporates and markets…In 2024, however, we expect more activity. Corporate uncertainty has dropped and there is greater visibility on the trajectory of economic and market indicators. The year may still include an economic slowdown but that may not be the key thing that drives markets.

One of the main reasons why the US managed to avoid a recession in 2023 is because consumers continued to spend. Of course, low unemployment helped but, even so, peoples’ desire to spend seemed to be in opposition to the concern they expressed in surveys.”

The US Consumer: Less Confident but I’m Still Spending

Source: Deutsche Bank

“What appears odd is the large gap between spending and consumer confidence. First, spending has been unrelenting. In real terms, US personal consumption kept rising in 2023 in line with its pre- and post-covid trend. Yet, at the same time, consumer confidence is in the doldrums as people recognise the cost of living has jumped.

When we look around markets now, it is hard to identify a specific major asset of consequence that may be in a bubble where investors are desperately trying to justify value. Sure, there are conversations to be had about weight loss drugs, olive oil, uranium, and bitcoin after their 2023 rallies. Yet, from a wider market standpoint, they are either niche assets or mere curiosities. Meanwhile, other major asset classes, such as certain equity indices, may have valuations that are ‘high’ by historic standards, but a ‘high’ valuation and a bubble valuation are two very different things.

There are some more serious arguments for a bubble in private credit. But systemic issues are unlikely in the near term. The $1.6tn of private credit assets represents barely 12% of the private capital market and barely scrapes the surface of the approximately $500tn in global financial assets.”

Fidelity

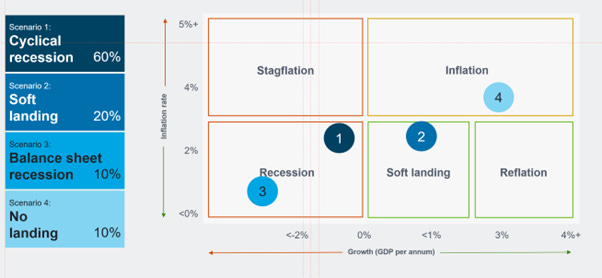

Scenario analysis seems to be popular these days with UBS (see part two of this round-up next week) offering a four-choice selection, as does Fidelity. This seems sensible to me and here is the Fidelity outlook:

Fidelity’s 4 scenarios for developed markets in 2024

Source: Fidelity International

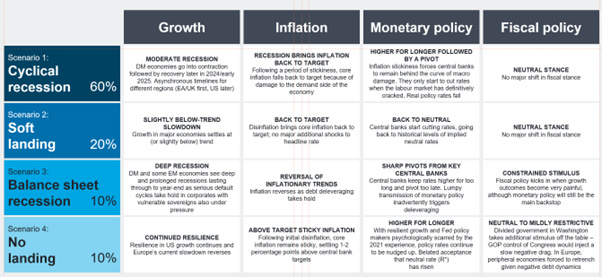

They provide further detail on each scenario in this chart:

Fidelity’s 4 Scenarios Detailed

Source: Fidelity International

They justify the favoured relatively bearish outlook by looking at business activity trackers, a $2tn estimated drawdown in personal savings through 2022 and 2023 and by easing in their own US Labour Market Tightness Indicator, which usually predates a recession.

Fidelity also offers a simple analysis of their favoured asset classes depending on the scenario:

Fidelity Favoured Asset Classes

Source: Fidelity International

In their recession scenarios, all sectors look negative except consumer staples, utilities and real estate which are flat or positive.

Goldman Sachs Asset Management

Goldman Sachs Asset Management (GSAM) focus on a few key themes for 2024, In Fixed Income, they suggest that “Bonds are Back but Focus on Quality”. Investors can earn 4-6% yield lending to high-quality companies, twice the 2009-2019 average, while they believe fundamentals in the US investment grade corporate credit market remain healthy,

They like disruptive technology, and believe that AI, Software, Healthcare, and Biotech hold promise:

“When beta is less likely to drive returns, alpha generation becomes even more critical. Allocations to selected large-, mid-, and small-cap technology names may be able to find secular winners underappreciated by the broader market…

Large pharmaceutical and biotech companies are outsourcing some core business functions…

In public markets, biotech has sold off indiscriminately, back to valuation levels not seen in 15 years. The number of small-cap biotech companies trading below balance sheet cash creates M&A targets for acquirers.

Potential sustainable investment returns are…increasingly competitive. Transition and “improver” funds are providing capital and financial incentives for high-carbon industry leaders to step up decarbonization efforts. Clean tech companies are compelling, particularly given the pull-back in valuations this year.”

GSAM are also promoting private equity and credit – fees are obviously a consideration.

Goldman Sachs Economics

Main points to take away:

Inflation nearing target, no imminent US recession, but markets already priced for soft-ish landing.

A benign growth backdrop in most places, but US looks to be the “surest thing”.

Higher rates cause ongoing stress for some sovereigns and pockets of corporate and consumer sectors.

Duration more attractive for portfolios.

Equity valuations not uniformly stretched, potential upside if rates fall earlier.

I shall cover the remainder next week as this post has already been twice my usual length. Premium subscribers can read on for access to a folder with the original reports (including those I’ll cover next week).