My Biggest Issue With “Quality Growth” Stocks

Plus: ChatGPT’s investing hot buttons and some excellent stock pitches

I had been to lots of Value investor conferences but never to a Quality Growth conference so I was curious to learn how these investors would describe their investment criteria at a recent London event. Almost all of the 14 fund managers talked about their process and there were some common themes, as you might expect. I noted their marketing “hot buttons” in the table below:

Quality Growth Themes

Source: Behind the Balance Sheet from Manager Presentations

As you can see, a focus on competitive advantage was near universal. This was variously described as durable, sustainable, or differentiated. If you had asked me going in, I would have guessed that the presenters would say a quality business would be likely to have high returns and would therefore have some form of moat, as Buffett described barriers to entry or competitive advantage. Yet returns was a much less frequent factor cited than I had expected in the marketing pitches.

Almost as popular as competitive advantage was growth which was defined in different ways. Only half of the managers thought valuation was important enough to mention – this could be because half don’t worry about valuation – indeed the presenter from Baillie Gifford downplayed valuation as a criterion, suggesting that the big winners will always appear expensive, which of course can be an issue with this investing focus.

Similarly, I cannot imagine that any of the investors wanted to invest in bad management, highly leveraged businesses or unsustainable businesses so the lower rating of these factors is probably more indicative of the marketing department’s emphasis than the managers’.

The Chat GPT View

I then asked Chat GPT for a list of hot buttons to use in a new Quality Growth Fund and got this response:

“Here are the most relevant and significant factors for identifying quality and growth stocks. These criteria should help you narrow down your stock selection process:

Earnings Growth: Strong and consistent earnings growth is a primary indicator of a growth stock. Focus on companies with a history of increasing earnings.

Revenue Growth: Look for companies with consistently growing revenues, as this often supports earnings growth.

Profit Margins: Analyze profit margins to ensure that a company can generate profits efficiently, and assess whether these margins are improving.

Competitive Advantage: Companies with sustainable competitive advantages, such as strong brand recognition, technological leadership, or network effects, are more likely to grow consistently.

Free Cash Flow: Positive and growing free cash flow is crucial for funding growth initiatives and returning capital to shareholders.

Management Quality: A capable and visionary management team is essential for executing growth strategies effectively.

Industry Trends: Consider whether the company operates in an industry with favorable growth trends and whether it can capitalize on them.

Scalability: Evaluate whether the company's business model is scalable, allowing for growth without proportional increases in costs.

Innovation and R&D: Companies that invest in innovation and research & development to create new products or services are often better positioned for long-term growth.

Valuation: While growth is important, ensure that the stock's valuation is reasonable relative to its growth prospects. Overvalued stocks can be risky.

Market Leadership: Leading companies in their industry, or those gaining market share, often indicate strong growth potential.

Sustainability and ESG: Consider environmental, social, and governance (ESG) factors, as they can impact a company's reputation and growth prospects.

Risk Management: Assess how the company manages various risks, including operational, financial, and market risks.

Chat GPT gave a pretty convincing list of factors. It’s clearly easier to come up with a convincing set of labels for a quality growth strategy, but it’s much harder to execute. The question - what is a sustainable competitive advantage, and how long will it last – is really difficult to answer in practice.

This subject merits a whole article and I intend to return to it. I will return to the conference because some of the other presenters were worth your attention. There were some interesting ideas and a number of names new to me, although the stocks chosen were not universally popular - I wonder whether many attendees felt like one of my friends who told me he didn’t pay several hundred quid to hear two fund managers telling him to buy Hermes at what is probably an all time high for its valuation. Although I did learn two things about Hermes:

1) They are increasing supply – a new workshop a year until 2026 vs 2 in the 2015-2020 period

2) One of the IR pros from a US fund was carrying a Birkin at the conference

I know a few women who like to carry a Birkin and I am guessing it will take quite a lot to persuade them otherwise and price really isn’t an issue. But the stock is now on 46x earnings and 29x EV/EBITDA, although the FCF yield is still 2%. I am not sure I would rush to buy it today:

Hermes Valuation

Source: Sentieo

Footnote: I checked with my go-to source for fashion advice, one of my personal expert network. And owner of several Birkins. This was the text exchange:

A Birkin Owner’s View

So perhaps the pricing power is intact…

But I wanted to talk about a presentation which challenged some of my preconceptions. Baillie Gifford’s Scott Nisbet’s presentation made me think. (In the interests of full disclosure, I should add that the firm is a client of Behind the Balance Sheet.)

Nisbet’s presentation was titled “Outrageous Growth at an Unreasonable Price” which is an interesting variation on GARP. The main points he made were:

There are very few stocks really worth investing in (the original Bessembinder study showed that 4% of US stocks delivered 100% of US market returns over a 90 year period);

These are growth stocks

It takes courage and fortitude to stay the course as there are always hiccups along the way

You need to focus on the long term and ignore the day to day noise.

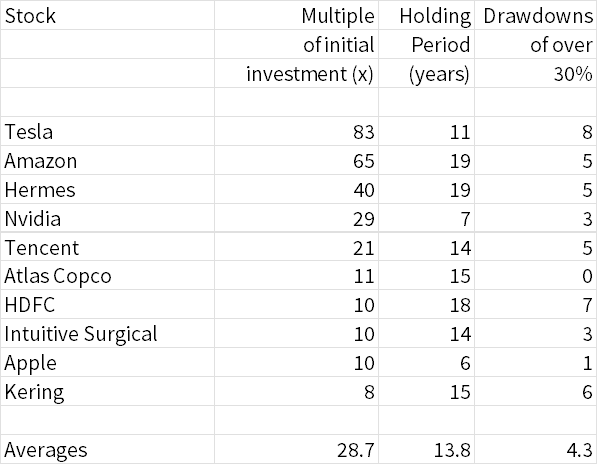

The table below illustrates the size of the gains and the degree of drawdowns suffered for their top 10 winners.

Baillie Gifford Global Growth Winners

Source: Behind the Balance Sheet from Baillie Gifford Data

Nisbet asked the moderator which of these was the biggest mistake – he didn’t know, but perhaps you do?

I immediately knew it was Apple, but it’s not obvious. Nisbet explained that they sold Apple in the mid-2010s as the turnover had reached $150bn. Their criteria for a growth stock is potential to double revenues in 5 years and the base rates indicated that Apple could not achieve this level.

(Note on base rates – the Base Rate Book by Michael Mauboussin who also spoke at the conference was published by Credit Suisse in September, 2016. It warrants a separate article, but it is a handbook of how fast revenues grow for most companies – ironically, companies like Apple and Amazon blew away the previous rates, for the first time in history for such large companies.)

Nisbet explained that Apple was a mistake – it would have been a 60-bagger. But once you have sold out, it’s really difficult to buy back in. This is a great illustration of how important it is to let your winners run.

They are forced by a limit of 10% in a single holding to trim some of their winners – they have trimmed Nvidia three times, for example. That limit was imposed 20 odd years ago and they would set it at 15-20% today.

Nisbet also highlighted that many of their clients are over-diversified. Their investment with Baillie Gifford is often but one of a number of growth portfolios and there will be index holdings and value holdings as well. Clients should give them more leeway – they have a more concentrated best ideas portfolio which only has 10 stocks and is allowed up to 50% in a single stock – it has delivered a better performance than their global growth portfolio.

The table above shows the top 10 winners. But they wouldn’t be able to show the losers on one page – that list would stretch for several pages. He cited Beyond Meat and Carvana as recent examples. Nisbet feels these are annoying but don’t matter. Many investors think of winners and losers as being binary which he thinks is a big mistake.

The most you can lose is 100% but the winners list above shows how large the gains can be. This is one of my personal weaknesses as an investor – I am too glass half empty and always worry about the downside – I should probably spend more time looking at the upside potential.

Nisbet explained that this is quite a normal phenomenon and that in their internal meetings to review a new stock, they only look at the upside in the first 30 minutes – nobody is allowed to vent the risks in order that the team can put the stock in a positive frame. I thought this was really interesting.

Paying subscribers can read on for the full list of stock recommendations and will get additional articles explaining the investment cases for some of the stocks and my takeaways in future weeks. If you are a paying subscriber, my mission is to ensure you will receive much better relative value than free subscribers going forward. If you are an investor, it’s honestly worth the $20/month.

And if you are serious about investing, we have opened the second cohort of the Forensic Analysis Bootcamp. Places are limited. Once October is sold out, the next session will be in February, at a higher price point. You can learn more and enrol here.