Investment Insights from Sohn London: A Tempting Trio

Why Spotify may continue its run and two potential multi-baggers

It’s Black Friday week. My marketing team like to make a one time discount offer on an online course to our lovely subscribers.

You can get 20% off How to Read a Balance Sheet, which has everything you need to know to understand and analyse financial statements. Use the code BF24.

This offer has limited availability and will only be open until Friday December 5. Premium subs get an even better deal behind the paywall.

Sohn London Conference

This year’s conference was especially good. There were 3 great short ideas and 11 longs, although one of those could have been a short. Speakers included two former partners of Chris Hohn’s TCI, long only funds, long-short funds, a private equity type fund, and a macro fund with a sovereign bond idea.

One quality growth stock was aired here before. I started to dismiss it, until I understood the presenter’s new angle and I am including that today for free subscribers. Premium subscribers get two stocks which could be rocket fuel for a portfolio.

Just to recap, the speakers were:

William de Gale Bluebox AM

James Hanbury, Lancaster IM

Anne-Sophie D’Andlau, CIAM

Liad Mediar, Gatemore CM

Edgar Allen, High Ground

Stephen Shields, North Rock Capital

Mikhail Zverev Amati Global Investors

Thiago Mordehachvili, Granular Capital

Diego Megia, Taula Capital

Oscar Hattink, BlueDrive Global Investors

David Semeza, Islander Capital Partners

Ali Benzakour, Envestra Capital

Malte Heininger White Creek Capital

Carson Block, Muddy Waters Capital

David Semeza of new fund, Islander Capital Partners, pitched Spotify which he had seen up 150%, driving his new fund to +83% as of the conference date. Regular premium subscribers may recall that this was pitched at the Quality Growth conference a few weeks ago by Angela Wu of Artisan Partners, in a presentation titled Unlocking Growth in Media.

Here is what I wrote last time when the stock was $367….

Spotify

I have written here about the relative valuation of UMG (Universal Music Group) relative to Spotify and why UMG deserves a greater share of the market cap assigned to the industry. My logic that relative profit pools in an industry today and going forward should drive relative valuations has cost me money. But I haven’t understood why I have been wrong.

Spotify continues to be a market darling and it has delivered – it had 31% of the global streaming market in mid-2021 and ChatGPT tells me that this data is also current (I don’t trust it, tbh):

Streaming Market Shares

Source: Artisan Partners from Midia Research, Q2, 2021

These shares are global, including China, and Spotify would have a larger share of the world ex-China. Revenues are c.$17bn today and it pays out 70% of its revenue to the labels, including UMG. Such payments trebled between 2017 and 2023 to $9bn. Wu explained that opex has ballooned from $1.4bn to a $4bn run rate in 2023 and has totalled $16bn over the last 5 years.

A new CFO coming from Saab is likely to look closely at the cost lines and lower losses in podcasting should help the gross margin trend. Spotify is growing share in the US and Wu reckons that music is under-monetised and looking at the relationship of music to video, that seems clear. Content owners want prices to increase and Spotify’s advantage is that it owns the consumer relationship so content owners are using Spotify to sell tickets and merchandise.

Their estimate of private market value is $467 per share and they believe that the business can compound at 15% and improve margins.

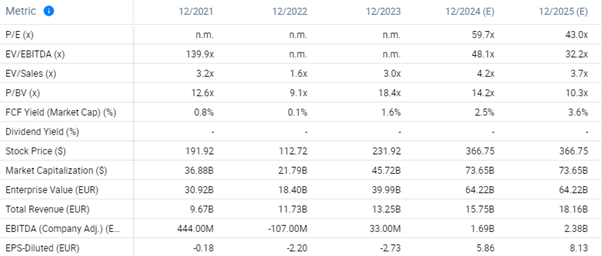

Spotify Valuation ($367) as of 27/10/24

Source: Alpha-Sense

I would expect stocks to trade at a discount to private market valuation and the then current price of $379 (the stock was up 3% the day I wrote) was at less than a 20% discount to their valuation. And the valuation was pretty steep - >30x EBITDA and 4x sales for a business with a 30% Gross Margin. I wrote I think UMG is cheaper and I have been wrong but I hope I will be proved right in the end.

Spotify Stock Price Chart to 27/10/24

Source: Alpha-Sense

Before I start on David’s pitch, which incidentally didn’t focus on the new CFO and the opportunity for cost-cutting, let’s first look at the valuation and stock price today:

Spotify Valuation ($477) as of 27/11/24

Source: Alpha-Sense

Yes, in a month, the stock is up 30% or $110 and stood at $10 above the Artisan private market valuation. Oh, to be a successful growth investor. I hope all my premium readers bought it, although I feel a bit stupid as I didn’t think it was cheap 30% ago.

Semeza believes it still has 27% upside at $470 which is c.$600 by end-2025. And here is the stock price chart:

Spotify Stock Price Chart to 27/11/24

Source: Alpha-Sense

Semeza is based on the west coast of the US and gave up an opportunity to be a professional soccer goalkeeper, but it looks so far that he has made the right decision. For those of you less familiar with soccer, it’s incredibly lucrative at the upper echelons. I was out with my kids and one of them asked if I had had a good week and I responded yes, that I had won a big contract. They kept pestering me to tell them how much and when I eventually relented, my elder boy laughed and told me that his team’s goalie made more in a week.

Semeza may be doing even better and his Spotify hypothesis is effectively that visionary founder Daniel Ek has decided that the time has come to inflect Spotify’s profitability much higher. Perhaps he is worried that earnings forecasts won’t support the share price (I would be).

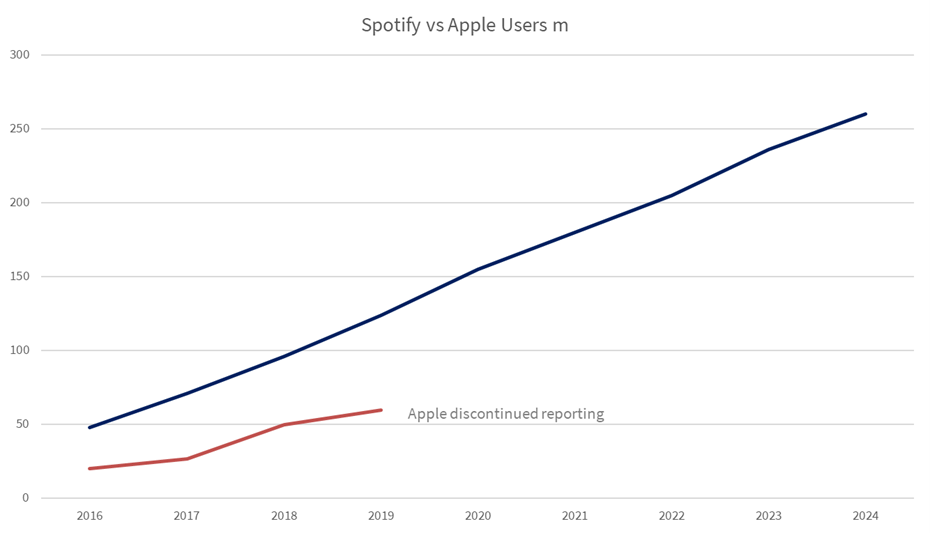

Ek is unusual for an S&P500 CEO in that he invests on a 10 year time horizon. Semeza sees Spotify as having much better engagement than rivals Apple and Amazon and I would agree with him that it’s a better product and it has a much larger share, but it doesn’t have any bundling opportunity without enlisting partners, so that’s necessary.

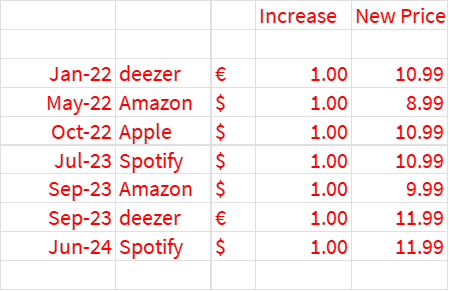

Source: BTBS from Islander Capital data

Spotify has had price increases in 2023 and in 2024 and Semeza believes it has gained power vs the music labels. I am not sure what evidence there is of that, other than its share price performance has been better – even if that’s true, it is in the price. But the trend of pricing is clearly up as can be seen in the table.

Music Streamers Price Increases

Source: BTBS from Islander Capital data

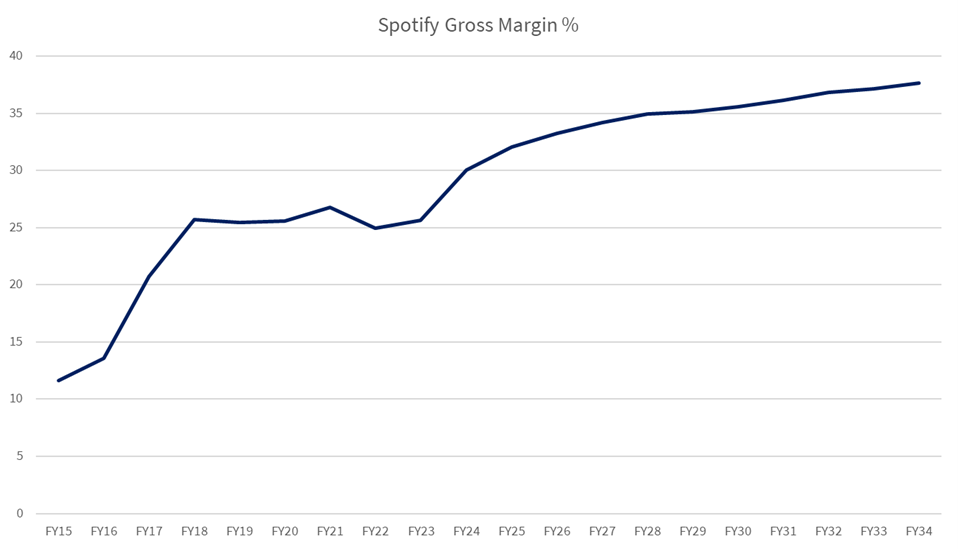

He thinks that gross margin will now pick up as the price is increasing for premium products including audiobooks. The chart shows that the analyst consensus expects Gross Margin which has been flat for 6 years to improve to mid 30s % from mid 20s % over the next decade. Islander is more bullish, forecasting Spotify gross margins of 37% in 2027 which is 3 points higher than the street.

Source: BTBS from Alpha-Sense data

To date, the music labels have taken a share of Spotify’s revenues, and Spotify has in the past benefited at the EBIT line from its economies of scale. But gross margin in the first three quarters of 2024 improved to 27.6%, 29.2% and 31.1%, which is impressive. Islander’s thesis is that the launch of audiobooks creates a potentially large new segment with much higher GM potential. They estimate that Amazon makes a 55% gross margin on audiobooks which is twice the music GM at Spotify.

This gives the stock much greater free cash flow support and they estimate that FCF margins will be 12% in 2024 and 18% in 2027 vs 5% in 2023. Consensus is 17% in 2027 and the FCF yield is then 4.5% per Alpha Sense (consensus Free Cash Flow data is not always reliable).

Their base case is $576 by end 2025 and their bull case is $864. Their bear case is a 4% FCF Yield and $293 which is a 22.5x EV/EBITDA. My portfolio isn’t up 83% year to date, so who am I to disagree, but if there is a bear case for Spotify, it may not stop at a 22x EV/EBITDA multiple. UMG is on less than that today.

Premium subscribers can read on for a rundown of some of the other (even better) conference ideas – I highlight 2 stocks which if the presenters’ convincing theses play out, should be 2-3 baggers over the next 18 months. Premium subs also get an even more generous offer on the courses.