How to avoid losing money

My favourite insight from a new investing classic

I am sure every reader of my newsletter will be familiar with what must be Warren Buffett’s most famous quote:

"Rule No. 1: Never lose money.

Rule No. 2: Never forget Rule No. 1."

Easier said than done of course.

But I have started reading what is undoubtedly going to prove one of my top 20 books on investing, “What I Learned About Investing from Darwin” by Pulak Prasad. Hat tip to my good friend Stu M for sharing.

Prasad manages a $5bn long only fund investing in quality Indian equities. I have only started this book but read the first 10% in one sitting. It’s impressive and Prasad’s philosophy is uncannily similar to this month’s podcast guest, Sebastian Lyon of Troy Asset Management. Both men have strict self-imposed imitations on what types of investment they will consider, with quality uppermost in their selection criteria. Prasad has 80 equities in India, Sebastian roughly 180 globally.

I would highly recommend both the podcast and this book. I enjoyed the first chapter of the book so much that I wanted to share with you the author’s brilliant analysis of the importance of not losing money.

Two Types of Investing Error

Prasad defines errors of commission and of omission as Type 1 and Type 2 errors. A Type 1 error occurs when you make an investment, thinking it’s going to be a winner and it turns out badly. A Type 2 error is when you fail to invest in something which goes up a lot.

I make a lot of both types of error. I have picked too many losers to list. And I have missed too many winners. Incidentally, although it’s a big mistake in opportunity costs, I don’t consider failing to buy Tesla as one of them. It was on a ridiculous multiple, was bleeding cash and the accounting policies where changing quarterly as they tried to minimise the reported losses. It may have been a 10-bagger since, but the decision I made at the time was correct according to my investing principles.

I really enjoyed Prasad’s explanation of how this works in practice and wanted to share this quote from the book with you. I need to preface this with the author’s assumption that there are broadly 4,000 stocks in the market of which 1,000 are good and 3,000 are bad investments:

“Let’s say you encounter a savvy investor who claims that he is right 80 percent of the time in his investment decisions…Stated differently, if he encounters a bad investment (i.e., one in which he will not make any money), he rejects it 80 percent of the time. If he sees a good investment (i.e., one in which he will make money), he makes a favorable investment decision 80 percent of the time.

Thus, his rates of type I and type II errors are both 20 percent. If this star investor makes an investment decision, what is the probability that it is a good investment? You’d say 80 percent, right? Wrong. The answer is 57 percent. But why? Isn’t he right 80 percent of the time? How can we go from 80 percent to 57 percent?

Here is how.

There are 1,000 good investments in the market, and since this investor makes a type II error 20 percent of the time (i.e., he mistakenly rejects 20 percent of these), he will select only 800 companies from his list. The market also has 3,000 bad investments, and since he makes type I errors 20 percent of the time (i.e., he mistakenly accepts 20 percent of these), he will mistakenly select 600 companies from this list, thinking that they are good investments. Thus, his universe of what he thinks are good investments will be 1,400 companies companies (800 + 600). Are you with me? Good. Now to the most interesting part. Of these 1,400 businesses that the investor thinks are good investments, how many do you think are good investments? Only 800. Hence, the probability of his making a good investment will be 800 ÷ 1,400 = 57 percent.

So here is the unfortunate conclusion. Even if an investor is endowed with the divine power of being right 80 percent of the time, the probability that he will select a good investment is only 57 percent. Even though he is “right” 80 percent of the time, 43 percent of his investments will turn out to be bad! The reason is simple, especially when we incorporate our prior knowledge of the business world: There are very few good investments in the market.”

From “What I Learned About Investing from Darwin” by Pulak Prasad. Reproduced thanks to the kind permission of the author.

The author goes on to explain how sensitive an investor’s hit rate result is to improvements in the two types of error. In short, avoiding losers gives you a much greater increase in the hit rate than improving your identification of winners.

Now, before explaining the arithmetic behind this, I should explain that although I intuitively knew this, I had never thought of it in mathematical terms before. This is the genius of this book - the author proves that avoiding losers is the right thing to focus on.

I have shown this in the two charts below. The first illustrates how your hit rate, shown in the red line, improves as you reduce type 2 errors (missing out on good investments). You get a reasonable improvement from 44 to 50%.

Effect of Reducing Errors of Omission

Source: Behind the Balance Sheet Based on Illustration by Pulak Prasad

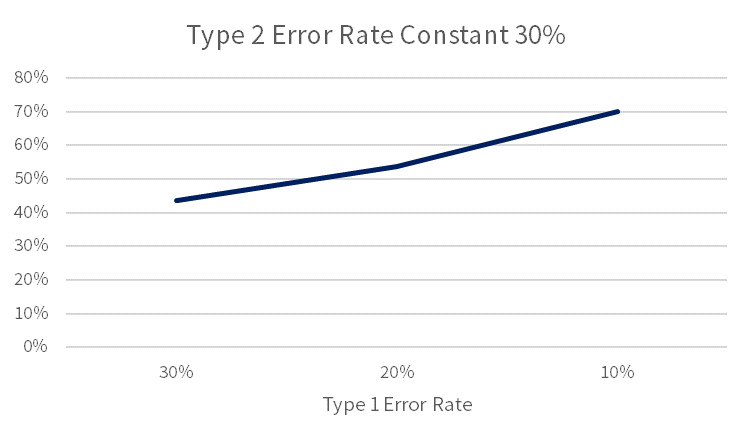

This is a nice improvement in the hit rate. But it’s not nearly as effective as reducing the other type of error – buying bad investments - as shown in the chart below: Here we go from the same starting point but end up at a 70% hit rate by cutting our errors by the same 20%.

Effect of Reducing Errors of Commission

Source: Behind the Balance Sheet Based on Illustration by Pulak Prasad

Therefore, the rate of improvement in making fewer errors is identical, but the impact on the hit rate is a multiple of the first case. In both cases, you start at the same poor starting rate of 44% but the same error reduction has a difference in hit rate outcome of 20 percentage points. That’s a huge differential.

Perhaps the reason I never tried to represent it in this way before is that I found this really hard to illustrate. Even with the benefit of Pulak’s excellent explanation, it was still difficult to draw the charts, especially writing this in an airport lounge at 1am, waiting for my connection.

But whatever the quality of my maths, the conclusion is clear – worry more about the risk of picking losers. The impact of such a strategy is far more powerful than I would have guessed. I came to a similar conclusion in my career by accident:

Loss Avoidance in the WIld

When I was at the hedge funds, I never worried about the ideas I missed as I always thought of ideas as similar to buses, miss one and another will be along in a minute. I was always much more concerned about downside risk.

A big loser means you require higher performance to recover – if you drop 50% on a position, you have to make 100% to get back to your starting point. And you don’t usually wait around at a hedge fund so you have to find something else to make the money back. And of course, you can get a lot of flak from colleagues and bosses and forego bonuses by screwing up.

I should add that one hedge fund manager I know gets incredibly upset at missed opportunities by his analysts, and is much more relaxed about their mistakes. I approve of not getting upset about mistakes because everyone makes them in this game. The analyst will already feel bad, so there is zero advantage in chastising an analyst for a bad call, whether they should have spotted it or not.

The Best Way to Spend Your Time?

The moral of this story is that picking bad stocks does more harm than missing out on big winners elsewhere. So perhaps the best time you can spend is in narrowing down your universe to a group of high quality stocks and then go to the beach (yes, I have a friend who does exactly this – you know who you are). OK, you might need to do a bit of work to ensure that they remain high quality and to watch out for ones which were becoming cheap or really expensive, but that is probably the best use of an investor’s time.

I had never thought about this in that way. So while I have never wanted to do a stock picking newsletter, I wonder if the publication of a global 100-200 stock universe would be something which people would find valuable. I may survey you on this, but feedback as ever is most welcome – you can reply to this email or email me on info@behindthebalancesheet.com.

Paying subscribers can read on for my modification to this approach, which I used to buy a quality stock this month. You might be surprised by the name.

Get Pulak’s book on Amazon UK or Amazon.com. Affiliate links, proceeds go to the Sohn Foundation, and don’t forget the Sohn Conference is on December 5 at the Marriott in Grosvenor Square. Hoping to have a few drinks there with readers.