How Buybacks Go Wrong

And a blue chip buyback that’s going wrong right now

I trust that my subscribers will all agree that buybacks are a good thing in the right hands.

From Mr Buffett’s 2023 letter: “All stock repurchases should be price-dependent. What is sensible at a discount to business-value becomes stupid if done at a premium.”

The arguments against buybacks usually centre on:

Do management know what they are doing in terms of capital allocation – ie are they buying at the right price?

Is the capital structure appropriate? Swapping equity for debt made so much sense when money was free in the 2010s, but less so today.

Is it effective on a societal basis or should companies be investing instead?

You will be relieved to learn that I am not going to explore any of these issues. Number 1 is a perennial question from readers and I may return to that.

Today, however, I want to talk about the mechanics of buybacks as companies aren’t always getting what they pay for.

Before we explore this, a quick reminder: My next Forensic Analysis Bootcamp starts on March 4. One recent attendee emailed to thank me as he came top in a case study in the recruitment process for one of the world’s top hedge funds. For more details and a full schedule of workshop topics, please go here.

From our Sponsor

Edelman Smithfield is a top financial communications firm, which specialises in reputation management and profile raising for financial services companies, and works with some of the biggest names in the investment world.

Every two years, they release their Asset Management Brand Index, a quantitative ranking of the strongest brands among the 50 largest global asset managers, based on input by investment consultants and allocators, and also a ranking of the 40 largest UK wholesale asset managers, based on input by IFAs and wealth managers. It is designed to help asset managers think forensically about the levers they can pull to improve their brands, show the trends impacting their clients’ perceptions, and demonstrate which firms are more successful than others in creating a positive identity.

The latest Index is now available. Visit www.edelmansmithfield.com/asset-management-brand-index-2024 to see the top line findings and request a copy.

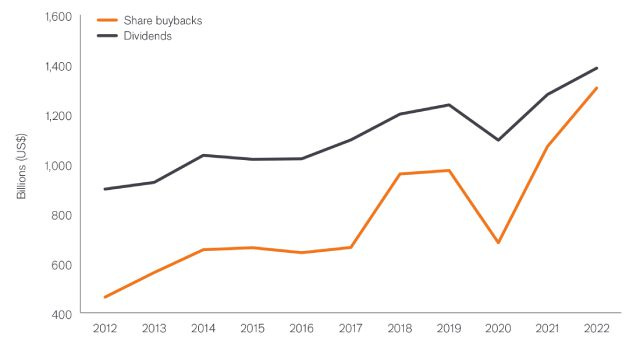

Scale of Buybacks

Buybacks are a big thing – a Harvard Law School Paper put the value at over $5tn in the last 5 years in the main developed markets. Janus Henderson put the number at $1.3tn in 2022 with buybacks closing in on the value of dividends globally.

Global Share Buybacks

Source: Janus Henderson

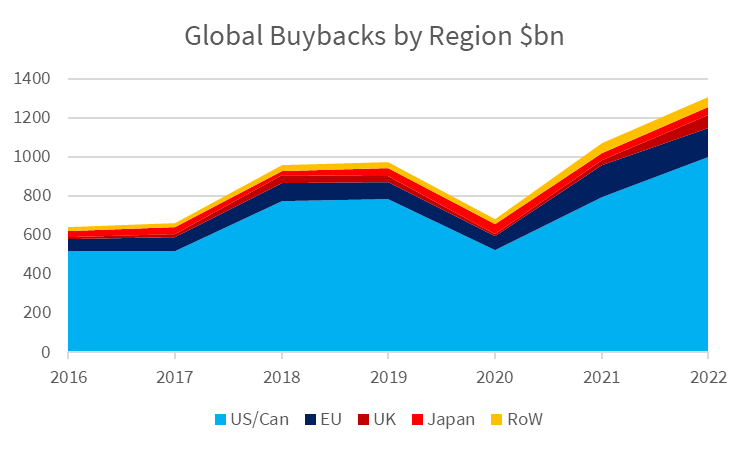

As you would expect, buybacks are most prevalent in the US but are becoming an increasing feature in Japan. Buybacks dipped in 2020 but have made up for it since. At nearly $1tn last year, the US dwarfs everywhere else and represents over ¾ of global buybacks, in spite of being under 60% of global market cap last time I looked. The RoW category in the chart below is Emerging Markets plus Asia Pac ex Japan.

Global Buybacks by Region

Source: Janus Henderson

Per Yardeni, the level of buybacks in the S&P500 has peaked, as interest rates have increased and with a less certain economic outlook. But they remain at a historically high level and there is no question that corporate demand is a significant component of the overall demand for stocks.

S&P500 Buybacks

Source: Ed Yardeni

Buyback Mechanics

When a company buys back its shares, they are then retired or held as treasury stock. If held as treasury stock, the shares repurchased lose their rights to voting and cash flows until they are reissued, while if retired they lose those rights permanently.

There are several ways to buy back shares - open market repurchase programmes are the most common followed by accelerated share repurchases (10%). Other rarer methods include tender offers and privately negotiated repurchases.

Tender Offers

Repurchase tender offers can be fixed-price or Dutch auction offers. In a fixed-price offer, the company offers to repurchase x number of shares at a price. If the number of shares tendered exceeds the offer size, the company can increase the size or buy back shares from tendering shareholders on a prorated basis.

In a Dutch auction, the company also repurchases shares at a single price, but this price is set at the end of the process. The company offers a range at which it is willing to buy back shares. Tendering shareholders indicate the lowest price they are willing to accept. The offer is executed at the lowest price which enables the company to repurchase its prescribed number of shares. The principal difference here is the company is required to make a firm commitment to repurchase shares.

Of course, management are in the hook here, but I don’t know why companies don’t use this method more often.

Private Repurchases

A privately negotiated repurchase usually involves the buyback of stock from a single investor, for example an activist who proposes that the company buys back his stock.

Open-Market Repurchases

Per Candor Partners, 90% of US buybacks are done in an open-market repurchase (OMR) programme. Companies generally do not adhere to a strict schedule when they repurchase shares in these programmes, nor do they buy back shares on every trading day or in every trading month. An academic study indicates that 24% of OMRs in the US (1985 – 2012) delayed the buyback until the following year.

Accelerated Share Repurchase

Accelerated share repurchase schemes account for c.10% of buybacks. Here the company contracts with a bank or similar to purchase a specific value of shares from a financial intermediary. Typically, the financial intermediary delivers a portion of this value in shares up front, which it borrows from large investors; it then covers the short position by buying shares in the open market over a period of time. The advantage to the company is an immediate transaction at a known price.

Disclosures

In the US, a company must announce its intention to conduct a buyback in advance and must provide quarterly disclosure on progress. In Europe, disclosures of purchases must be made within a week and in the UK with only an overnight delay.

I think advance warning of the programme is desirable as capital allocation is one of management’s most important tasks. (My personal view is that if the CEO decides to buyback the stock at a stupid price, I would like to know in advance as I might well decide that I don’t want to stick around, but will use this as an exit opportunity.)

Quarterly disclosure seems sensible, daily seems daft. I cannot think why regulators require UK companies to telegraph their intentions to the market – it seems likely to disadvantage the company and its shareholders. It also makes it easier for intermediaries to profit. These rules need revisiting, as the regulations should help shareholders, not market participants.

Execution Issues

Hopefully, this has painted the background. We all (hopefully) know that buybacks in the right hands are good and that there is a risk of value destruction. What I hadn’t realised is that the average buyback wastes a lot of shareholder money in execution.

I think the problem here is that the average CEO and CFO are easy prey for slick investment bankers who are profiting from their clients’ naivete.

One academic study found that an astonishing 68% of ASRs had no price cap or collar. I simply cannot understand how any CEO or CFO would sign off on that, although perhaps part of the problem is that buybacks are greeted with fanfare but are subject to only the most cursory examination – better disclosure would definitely help.

More common than ASRs are OMRs or Open Market Repurchase Programmes. This includes plain vanilla agency and similar programmes. Here, the company normally engages an investment bank to purchase a set value of shares, generally at a discount to a VWAP benchmark, over a period. This makes sense from the perspective of the management who don’t want to disrupt the share price by barging into the market and pushing the stock up, only for it to fall back. The risk for management then is that they buy at a premium to the prevailing price when the time comes to report to shareholders and they can then look stupid.

The standard practice of the engaged bank is to guarantee a discount on the average price over say 100 days. This has obvious appeal to the company’s management. The bank then has complete control over the pace of purchases.

These programmes are akin to averaging in and are perceived to reduce the risk of looking stupid. The idea of contracting with a bank to beat a benchmark seems perfectly sensible and incentivising the bank with a performance fee is normal practice. There can however be a problem with the way in which the performance fee is set and the way in which the price is calculated.

I am indebted to Michael Seigne of Candor Partners who explained all this to me in much greater detail. Michael advises companies on the execution of buybacks and is worth speaking to. Hopefully, he will be treating me to a lavish lunch when he has a queue of new customers (he should have).

One issue he has found, astonishingly, is that sometimes the price is not adjusted for dividend payments during the period.

Another is that some contracts allow the bank to specify the end of the trading period - for example, a period of 100-150 days might be used. This gives the bank a significant degree of flexibility. Let me illustrate with a coin tossing challenge. Obviously the odds of heads vs tails is 50:50. What the broker does here is offer the company a 51% guarantee, over a period of 100-150 days. The broker decides when the game ends and can stop at any time when the outcome is in its favour. The odds are stacked significantly in its favour – the same is true in a buyback.

These are not imaginary cases. Consider Royal Mail which initiated a £200m buyback in 2022. They purchased £184m of stock, paid under £1m in stamp duty and paid some £16m to the bank in fees.

IHG returned $500m of surplus capital but paid a £10m fee to their investment bank. A fee of over 2% seems too high for this type of activity.

It’s hard to know how prevalent this is because few companies offer this transparency. But with $6tn+ in buybacks in the west in the last 6 years, there has probably been a significant amount of value transferred from shareholders to Wall St.

Premium subscribers can read on for a real life example in which the buyback is being poorly executed and shareholders are paying the price.