To say the Moneyweek Conference 2023 in London was downbeat would perhaps be a misrepresentation. Many of the professional managers presenting were quite positive on the outlook for their funds and sectors. But for me, the two most interesting presentations of the day came from Ruffer and GMO and both were more than a little depressing. I will return to James Montier’s presentation in a future edition (it was brilliant) but l shall begin this week with the first keynote from Alex Chartres of Ruffer. He echoed many of the regime change themes I have been writing about for the last 18 months or so.

First, a word from our sponsor:

How can you increase ROI on your investment research spend?

Stream provides a 26,000+ expert transcript library, powered by AI search technology, and highly competitive rates on one-on-one expert call services. We can even arrange for an experienced buy-side analyst to conduct calls on your behalf. Traditional expert networks are dead, they just don't know it yet.

On to the conference…

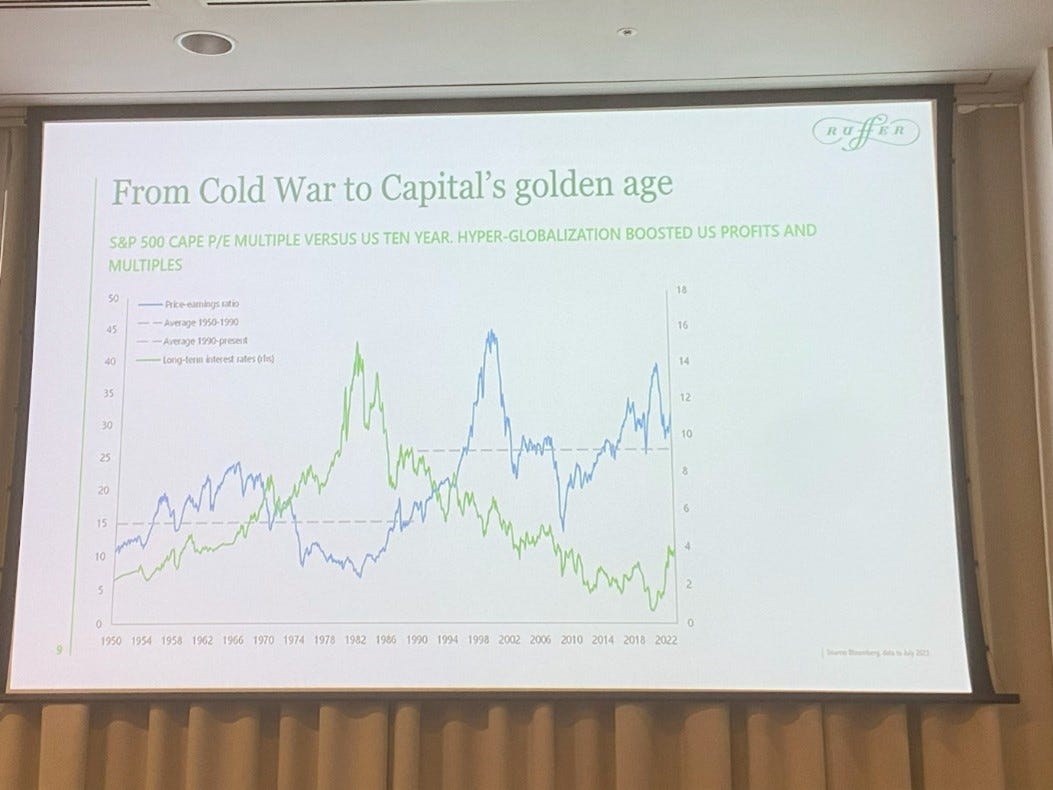

Chartres certainly didn’t start on an upbeat note. It was an impressive presentation and he opened by talking about how we had come from a golden age – he referenced China, Russia, tech, workers, globalisation, privatisation and other themes, as encapsulated by this slide:

You never had it so good

Source: Ruffer

The last 30 years have seen a much higher average level of CAPE than the previous 40 for all the reasons we know and have discussed here. One of these is the Cold War. Now there is a new world order and a new cold war. Niger has suffered its 8th coup with consequent risk to the uranium price and Chartres believes that China is preparing to invade Taiwan. (I wasn’t sure if this is a personal or house view).

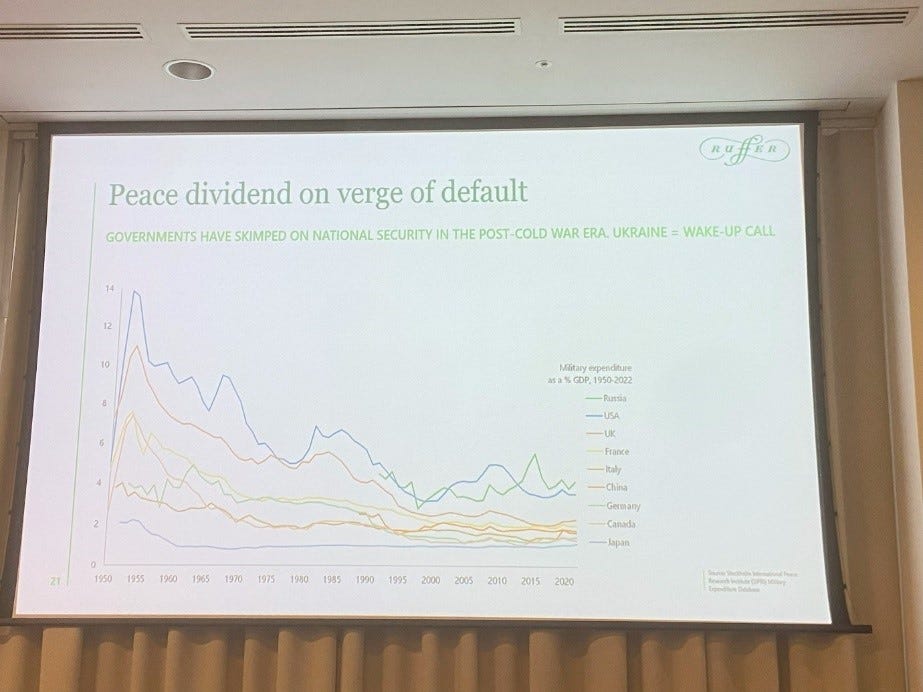

The Next Cold War

Source: Ruffer

Since the end of World War 2, the west has enjoyed a peace dividend and the invasion of Ukraine marks an end to that long period of decline in spending.

End of the Peace Dividend

Source: Ruffer

In 2024, there will be elections in the US, UK, Russia (!) and Taiwan – these bring additional risks.

China

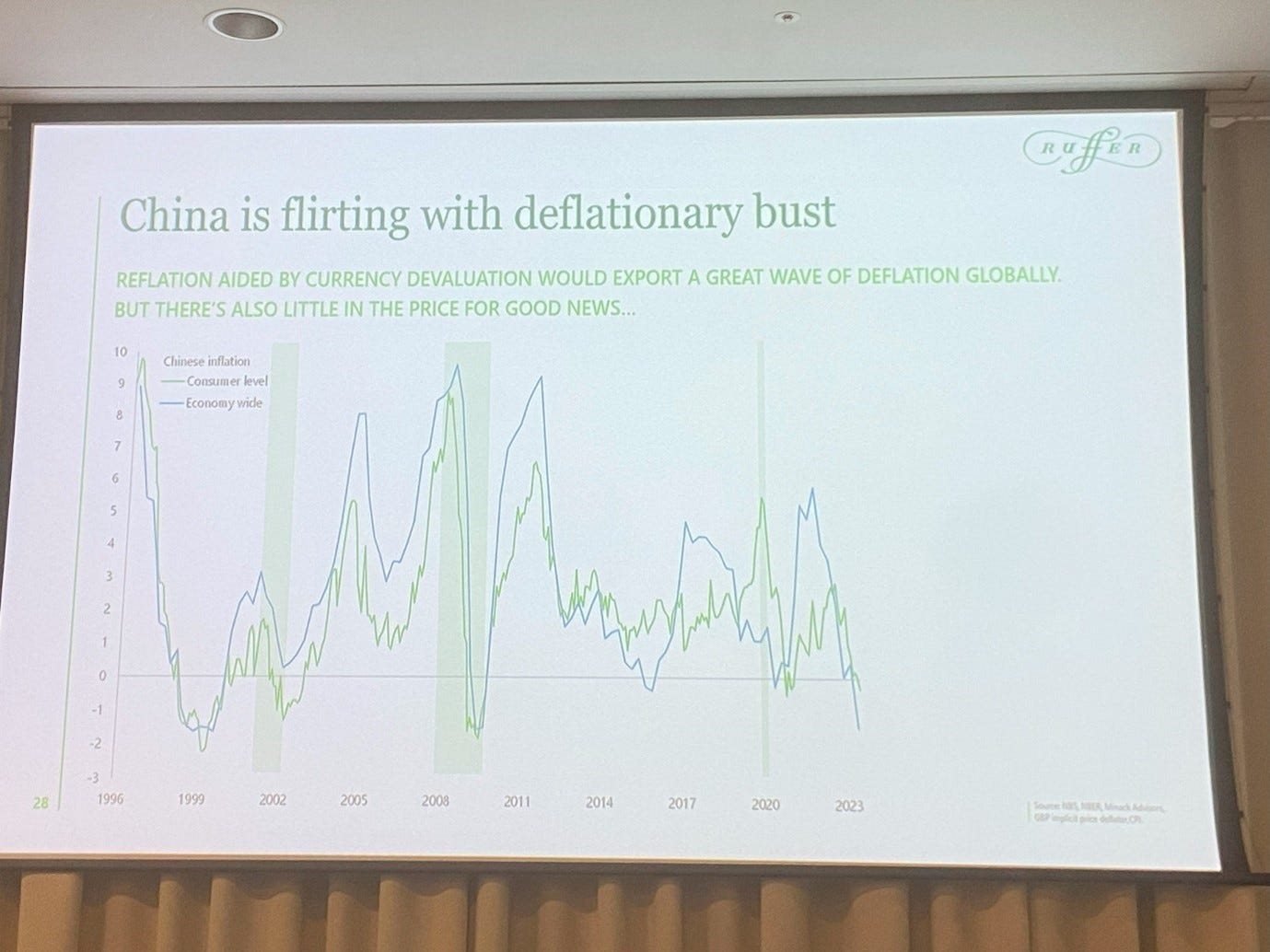

Meanwhile, Ruffer believes that China, in contrast to the west and just about everywhere on the planet, is suffering deflationary pressures instead of inflationary ones. The problems here are both immediate and longer term:

China Deflationary Pressures

Source: Ruffer

The immediate one is property – he referenced Country Garden which had suspended trading in 11 bonds and has since suffered further setbacks. It recently missed a payment of just $60m and announced that it “will not be able to meet all of its offshore payment obligations”. The FT reported that company has $10bn in US dollar debt alone and around $200bn in liabilities.

Property is an immense problem here because Ruffer estimates that 80% of Chinese wealth is effectively tied to property – if that train goes off the rails, then there are serious implications for the economy at large. Mixing metaphors, sorry, it does seem like it has already run off the cliff but like Roadrunner, just hasn’t yet looked down.

A longer term issue is demographics – the population in China will halve by the end of this century.

Other Issues

Climate Change: Net zero is commodity intensive – an EV uses 7x a conventional car’s volume of rare earths. Ruffer like commodities and the speaker asked if there could be an OPEC for metals – Brazil, Chile, Peru and S Africa.

Demographics represent another headwind as fertility rates are in decline and the ageing population creates a potential public finance crisis. If you look at say France, the growth of the population over 65 years is massively higher than economic growth.

Return of the Big State was another theme. The Inflation Reduction Act is already stimulating investment but the state spend is the top of the iceberg as it will fuel 10x the federal outlay in private sector spend. Which means a clean tech capex boom is coming.

Financial repression is inevitable - the Congressional Budget Office is projecting debt:GDP at 190% in the US by 2050. Oddly, higher real rates have not yet fully impacted markets where inflation expectations remain low. This creates an asymmetric opportunity. If you bet on higher inflation, if nothing changes you don’t lose much but if market perception changes, you can profit handsomely.

Here is Jonathan Ruffer on inflation in the firm’s latest quarterly:

“It is our firm conviction that inflation is in an inexorable up-cycle. We do not put timings on it, but two factors will prove more powerful at stoking rising prices than the single force pulling the other way – the impact of central bank tightening. The first is the increased balkanisation of economic activity – the extraordinary growth of China, funded by two decades of free American money, gave the developed world a holiday from inflation. That has ended. The middle-aged investor class were the unambiguous beneficiaries, the younger workforce the opposite.

This inequality has led to the second key driver of inflation: a reversing of the Marxian battle between capital and labour, something that always happens at extreme points, typically reached every half century or so. The bottoming of interest rates in late 2021 was the nadir of labour, and the onset of strikes by organised labour will be a feature for the next couple of decades, and probably longer.”

Conclusion

Chartres concluded that the biggest risk for investors in inflation and financial repression. The regime has changed. For 30 years, politics didn’t matter, it was all about profit. Bonds were negatively correlated to equities in a 40 year bull market. But if inflation is higher, bonds may not offset equities because looking at a longer timeframe, it was normal for bonds and equities to be positively correlated.

To preserve your wealth, you need to

be more active: buy and hold won’t work

mind the tails, be anti-fragile

own real assets

This is very much in line with what I have been saying for the last 18 months. I have been presenting on this at various investment conferences (and happy to do more – get in touch). It’s a comfort that smart investors like Ruffer are in the same camp.

Chartres talked about “lobster pots” – stocks which were easy to get in, hard to get out. Here are a few of their favourites:

Ruffer Lobster Pot Stocks

Source: Ruffer

Not all of these are publicly quoted and honestly, I have no idea why Ikea and Lego are on that list. There are quite a few stocks there that are over-owned and a change of sentiment could cause an abrupt reversal. China is a major factor in many of them.

Chartres was going pretty quickly so I only had time to examine the slide more closely now and I am not sure I get it. I have recently had some merch produced, so a prize of a baseball cap or a polo shirt to the best explanation of this slide. Email btbscompetition@gmail.com.

Finally, our second Forensic Analysis Bootcamp starts tomorrow, October 16. We are at capacity but if there is anyone who is a newsletter subscriber who has forgotten to join, you can sign up here before 17.00 UK time on October 16.

Paying subscribers can read on for Chartres’ recommendation on two $1tn+ stocks which I think is spot on.