Aston Martin's £142 million hangover

"Or why I prefer my finance chiefs to be old, grey-haired and conservative

In my previous look at Aston Martin, I covered the latest fundraising and looked at the treatment of capitalised R&D. This time I want to cover the other intangible assets. These are often overlooked by analysts, but I believe the treatment of such assets often gives a clue as to the psychology of the chief financial officer or finance director.

I like my finance chiefs to be old, grey-haired and conservative – they usually don’t like to have too much in the way of intangibles, perhaps some goodwill and similar acquisition-related assets, but not much else. Aston apparently employs a racier type of finance specialist, judging from its Intangible Assets note.

Aston Martin Intangibles

Source: Aston Martin 2021 Accounts

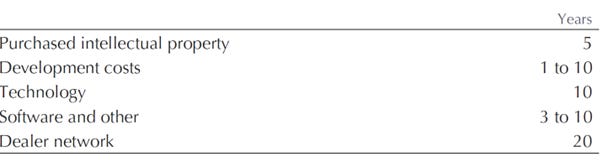

As I pointed out last time, the company is carrying £1.4bn of intangibles on its balance sheet with a gross cost of £2.2bn and an amortisation last year of just £135m. We looked at the capitalised development costs then, so let’s now take a closer look at the other intangible assets.

Starting at the right with software, the company has £67m of capitalised software, only added £4m last year and wrote off £3.5m – the net book value is just £10m. The accounting policy is a life of three to 10 years, which sounds rather long. Software is mentioned only three times in the annual report – first is “the business has renewed its focus on in-house intellectual property development, including software and skills relating to electric vehicles, thereby fostering engineering excellence within our corporate DNA”. The other two are accounting policies and this note.

Aston Martin Amortisation Policy

Source: Aston Martin 2021 Accounts

Perhaps the company is making immense investments in software and writing it all off through the P&L. In which case, why capitalise anything? I cannot conclude anything from reading this part of the note, but if I were still at a hedge fund, I would be asking Investor Relations what the £4m represents, what is the total spend and is the company investing enough?

Working from right to left, the second asset is the dealer network, £15m gross and £5m net. Formerly this was lumped together with software, which was quite confusing. Depreciation is £0.7m, consistent with the 20-year life in the accounting policies note. The network has a further 6.5 years of amortisation and it’s possible that Aston could still be around in 2030. But it seems an unusual asset to be carrying on your balance sheet and I wonder how they derived its value.

Aston today has more than 160 dealerships in 53 countries. It presumably had fewer when the asset was initiated, but it puts a value of about £100,000 on a dealer – or less than the value of the average demonstrator. To be clear, I am not advocating that they should increase the value of the asset, just wondering what a dealership might be worth to the company. I would have thought that there were candidates queueing up to sell Aston Martin cars.

We covered the capitalised development costs last time. I will come back to the technology. Goodwill is straightforward and not a large number. The brand is on the balance sheet at £300m, which doesn’t sound a lot for a global luxury brand – the #100 brand (Colgate) is valued at $19bn – but is significant in the context of £1bn annual revenue and not much in the way of profit in the past few years (and probably in the entire brand’s history).

Development costs are an interesting element. Here is the note which explains the transaction leading to the appearance of this asset on the balance sheet, with the key text in italics:

“On 7 December 2020, the Company issued 224,657,287 shares to Mercedes-Benz AG (“MBAG”) as consideration for access to the first tranche of powertrain and electronic architecture via a Strategic Cooperation Agreement. The Group was required to undertake a valuation exercise to measure the fair value of the access to the MBAG technology upon its initial capitalisation. The Group selected the “With and Without” income approach which compares the net present value of cash flows from the Group’s business plan prior to (“without”) and after (“with”) the access to the technology. This methodology estimates the present value of the net benefit associated with acquiring the access to the technology. In the Group’s assessment, the fair value of access to this technology is £142.3m. The £142.3m represents the assumed cost at acquisition after which the cost model will be adopted. Amortisation is aligned to the expected pattern of consumption of the economic benefits.”

So the group valued an agreement with Mercedes to supply it with powertrains and electronics at £142m. They issued shares to Mercedes in return, so they had to do something with the cost – either capitalise a notional asset or charge it as an expense. Given that there is a life to the agreement, spreading the cost over several years seems logical. But over how many years?

Rebadged Mercedes Engine

Source: Car Throttle

Note that there was an existing balance in technology, prior to this agreement, valued at £21.2m gross. The related amortisation has been £1.9m a year for the past few years, implying a life of about 11 years. We don’t know what technology this is, but it has an unusually long life – a car model usually lasts seven years and technology usually has an even shorter life.

The co-operation agreement is, I believe, a controversial issue – there is no amortisation being charged. Consider this from the perspective of Mercedes. They could have sold Aston Martin engines at say £10,000/unit, but instead Aston gave them some shares and they agreed a lower price for the engines, let’s call it £9,000. Unless you charge the cost of these shares somewhere, Aston ends up making a magical £1,000 extra profit per car.

The notes continue: “In October 2020 the Group entered into an expanded and enhanced technology agreement with Mercedes-Benz AG contingent on shareholder approval, anti-trust and underwriting conditions. This Strategic Cooperation Agreement gives the Group access to powertrain architecture (for conventional, hybrid and electric vehicles) and future oriented electric/electronic architecture for all product launches through to 2027.”

Perhaps Aston Martin is not yet using any of the Mercedes powertrain architecture covered by the agreement – I believe they have used Mercedes engines for some time, predating the agreement. So it’s possible that they are not required to amortise yet. Let’s say they start in 2023 – then they will have an amortisation charge based on the life of the models launched in 2023-27. If the model life is say seven years, then the amortisation charge should average about £12m a year (£142m over a 12-year (7+5) period), but will start lower and end higher.

And here’s the thing – previously, I pointed out that investors failed to appreciate the impending cliff for earnings when the R&D amortisation kicked in – this co-operation agreement is similar. In both cases, there is no impact on cash flow, only on the optic of earnings and the P/E metric. The popular EV/EBITDA measure ignores this parameter. But in my view, the treatment indicates a company where accounting conservatism may not be top of the agenda; they rarely make good investments.

I also wonder about the cachet of a £150,000 sports car which has an engine from an S-class Mercedes, but I am a bit of a purist when it comes to cars.

Next time, I shall discuss the liquidity issue, which was the other red flag at the time of the IPO and was the real killer when it came to assessing the IPO opportunity. For paying subscribers, the Aston model is attached, plus a coupon for a free investing course.