Are you really a long term investor?

Looking at 123 year returns

Welcome to the over 1000 new subscribers joining in the last week, the best week since I started this Substack. Thanks! Let me know how you like the content.

Greetings from Bahrain. I had an interesting visit this week to train 40+ bankers in how to spot frauds. I didn’t get much time for sightseeing, but was impressed with the country and looking forward to a return visit. Some amazing architecture and I gleaned some interesting insights into the economy where finance is a key industry.

Podcast

Regular readers know that I produce a monthly podcast which has had some star guests – not always the best-known personalities, but some really thoughtful people and some fascinating conversations.

This month features Gavyn Davies, the former Chief International Economist for Goldman Sachs, former Chairman of the BBC and current Chairman of Fulcrum Asset Management. I met him for the first time doing this interview. In my research, I discovered that he was the co-founder of 4 multi-billion asset managers, which surely must be a record. I discovered what this attests to – he is not only super smart, as you would expect, but he is also a thoroughly nice man.

I really liked two things about Gavyn – first, he is incredibly measured and thoughtful in his analysis and responses to questions. Second, he has his feet on the ground - in spite of obviously being very rich, he takes the bus to work. Apart from his thoughts in markets and economies, it’s definitely worth listening to his analysis of the UK political backdrop and the importance of public service broadcasting.

Last month’s guest was Tian Yang, who I would guess is half Gavyn’s age, but is nevertheless a formidable intellect. I was impressed with his knowledge and understanding of global macro and by the sophistication of his analytical approach. Regular readers know that I am a huge fan of the capital cycle approach, popularised by Marathon Asset Management in the books Capital Account and Capital Returns, both edited by Edward Chancellor. Tian is the first person I have encountered who has developed a quantitative application of the strategy – you need to listen to his explanation.

Please do listen to these two episodes and let me know what you think – and if you enjoy them, a 5* rating on Apple Podcasts helps spread the word – thanks!

Credit Suisse Annual Returns Yearbook 2023

Regular readers will also know that I like to look at investment on a longer term perspective. And when it comes to markets, the longer the better. This is particularly true today, as we have passed an inflection point:

the last 40 years have been characterised by falling bond yields and rising valuations

we don’t know what the future holds but we know it’s highly unlikely to look like the last 40 years.

The last column I wrote on this subject looked at returns from equity and bond markets in the last 100 years or so, drawing on research presented in Russell Napier’s History of Financial Markets course. I therefore looked forward to the publication of the Credit Suisse Global Investment Returns Yearbook, compiled by respected academics Dimson, Marsh and Staunton.

Chapter 2 outlines the long-run returns on stocks, bonds, bills, and inflation since 1900. It shows the long run performance of equities relative to bonds; looking only at the last 40 years obscures some oof these characteristics. It also highlights that higher levels of inflation bring lower performance from stocks as well as bonds. Although equities are an investment in real assets, they don’t provide inflationary protection. It also shows the impact of cycles of increases and reductions in interest rate on stocks, bonds and risk premiums.

One benefit of looking far into the past and comparing with the present is that it illustrates just how much things can change. Obviously looking back over 100 years, you would expect to see significant changes, and for example, it would be obvious that the US wouldn’t be the largest market in the world, with that title belonging to the UK. Before you look at the table below, if I told you that today the US market was nearly 60% of the world’s capitalisation, and the UK was under 5%, what would you guess the numbers were in 1900?

The authors estimate that the US is now 58% of the world market cap, with Japan at 6.3% and the UK at 4.1% followed by China at 3.7% and France at 2.8%. At the turn of the last century, The UK was 24% the US 15%, Germany was 13%, France was 11.2% and Russia was 5.9%.

World Top Markets by % total Market and Position

Source: Credit Suisse Annual Returns Yearbook 2023

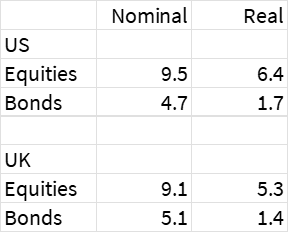

Returns from the US market beat those in the UK where they estimate inflation as 3.6% pa, higher than the 2.9% in the US.

Annual Returns % from Equities and Bonds US vs UK

Source: Credit Suisse Annual Returns Yearbook 2023

The equity returns from the US of 6.4% pa real compare with the world ex-US of 4.3% pa, the world overall of 5.0% pa and developed 5.1% vs emerging markets 3.8%. I was surprised that EM had not done better in a 123 year trend, given it was starting from a lower base, presumably had better economic growth and obviously had much higher volatility – maybe my bets today are misplaced?

There is a huge dispersion of returns and countries which suffered in wars generally show the worst equity returns and the highest volatility of those returns which is as expected. Bonds delivered negative real returns for several of those countries – Austria, Italy and Belgium occupying the bottom three spots, but even in those countries, real equity returns were positive – albeit “just” 1-2% pa.

The yearbook also analyses real returns from equities and bonds vs real interest rates and as perhaps might be expected, when rates are low, returns are low. Negative real interest rates were experienced in around one third of all country years, and the table charts the performance of equities and bonds in real terms for various bands of negative rates:

Annual Real Returns % from Equities and Bonds in Periods of Negative Rates

Source: Credit Suisse Annual Returns Yearbook 2023

These periods of negative real rates mainly occurred in inflationary times and this is likely what we should be thinking about now. The authors use this data to predict what the world may look like for Generation Z and they predict real returns of 4.0% pa from equities and 1.5% from bonds. This is significantly worse than the 6.7% real return pa from equities and 2.9% pa from bonds experienced by the baby boomers, but is perhaps not as bad as might have been feared.

Interestingly, the authors have revised up these expectations since last year as the dismal returns in 2022 have increased expectations for the remaining future years.

They also discuss inflation and cite academics Arnott and Shakeria’s work suggesting that inflation may prove more persistent than many hope – getting to 3% inflation from 8% and above has historically taken on average over ten years. This might be a worst case outcome, but they suggest that a return to low inflation is very much a best case outcome. Obviously the ten year period is influenced by experience in the 1970s and no cycles are identical, but it seems madness to me not to have some inflation hedge in portfolios.

We know inflation is bad for bonds and there is plenty of academic work suggesting that it’s bad for equities with markets in the 1970s providing strong support. Although equities are an investment in real assets, inflation erodes margins and the associated higher interest rates undermine valuations.

The authors suggest that commodities have been a poor long term investment with an average real return of -0.5% pa. But an equally weighted portfolio of commodities has beaten bonds with a 123 year return of 12x vs 7.8x for US bonds and just 0.9x for the average commodity. Of course this is before costs which are significant for commodity investors as there is the cost of physical storage. The authors suggest that futures contracts deliver 3.3% annual returns but I wonder if the cost of the roll has been fully factored in. Gold has outperformed cash but with higher volatility and has underperformed US bonds significantly over the very long term.

The attraction of commodities, commodity futures and gold is that these three asset classes are all positively correlated with inflation while every other asset class, including real estate, is negatively correlated. The authors are less keen on commodity equities but for the private investor, this might be a more practical alternative to a portfolio of commodity futures.

I haven’t yet received the full yearbook (a physical publication) and have only read the choice extracts published on the web, but this long history is something worth revisiting each year as we enter this new world which seems certain to be very different from the last 40 years. There isn’t that much new in here, but it’s helpful to see data to support an argument.

Paying subscribers can read on for a link to my podcast with Grant Williams. I know there are a lot of free podcasts out there but his subscription podcast is just $10/month and I recommend it.