Are we back to 2000?

Fundsmith on Concentration, AI and the Psychology of Underperformance

Introduction

This week, my report from the Fundsmith meeting, the nearest UK counterpart to the Berkshire AGM. In spite of a lengthy period of underperformance, I think it’s still worth listening to what Terry Smith (a recent podcast guest) has to say.

Fundsmith Meeting

Fund holders were greeted by an almost life-size version of Terry. This remained intact, although many of the people I spoke to at the welcome drinks were baying for his blood, after 5 years of underperformance and negligible returns last year.

He made a good job of defending himself. He described his 2025 performance as “poor” and

“if we keep going like that, we will be poor”

He pointed out that 5 years ago, the fund did 22% vs the market at 22.3%. He doesn’t count that and he dislikes commentators describing him as making excuses – he believes that it’s up to him to explain the performance and up to the fund holders to decide when to buy or sell.

He did a brilliant sales job, pointing out that selling a fund after it had underperformed was the worst thing you can do:

When to Fire a Manager

Source: Fundsmith from Cambridge Associates Data

The manager you fire after underperformance goes on to outperform as soon as you fire them, while the manager you hire after years of outperformance goes on to underperform. It’s well-known that switching usually happens at the worst time. Here is Cambridge Associates on the subject:

“Recent manager performance, even over the intermediate term, is a poor guide for hiring and firing decisions. A study by research firm Dalbar found that over the 30 years ended in 2023, the average US equity investor detracted more than 2 ppts annually due to behavioral issues, such as firing managers near their lows and hiring after strong performance.”

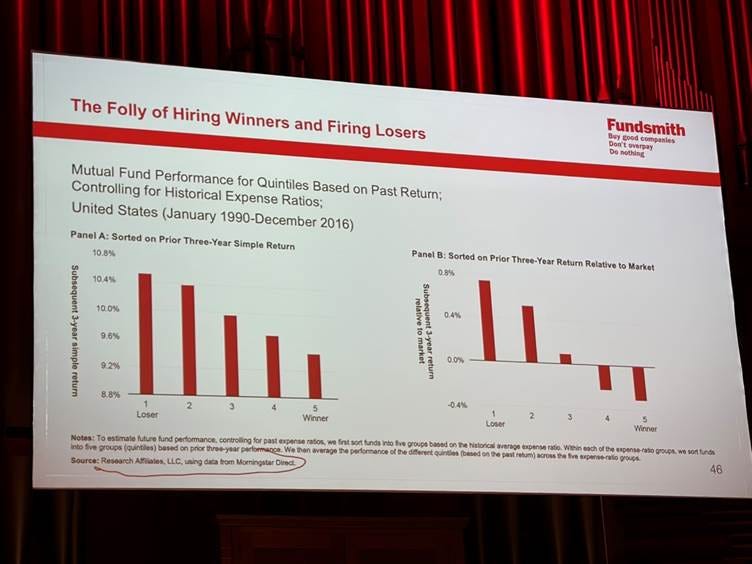

Tery went on to show the following slide, further proof that past performance is not necessarily a guide to future returns.

Firing Losers may not be a Good Strategy

Source: Fundsmith from Research Affiliates Data

The people I spoke to hoping for an apology were disappointed, but they got something more interesting - a lesson in how distorted today’s markets have become. Terry made the point, also made by Simplify’s Mike Green (see my article on my Berkshire trip last year) that flows now matter at least as much as fundamentals. He referred to the study “The Inelastic Markets Hypothesis” from Gabaix and Koijen: in an inelastic market, flows in and out of equities move prices disproportionately. $1 of new money flowing into a stock can add $5 ($3-$8) to its market cap.

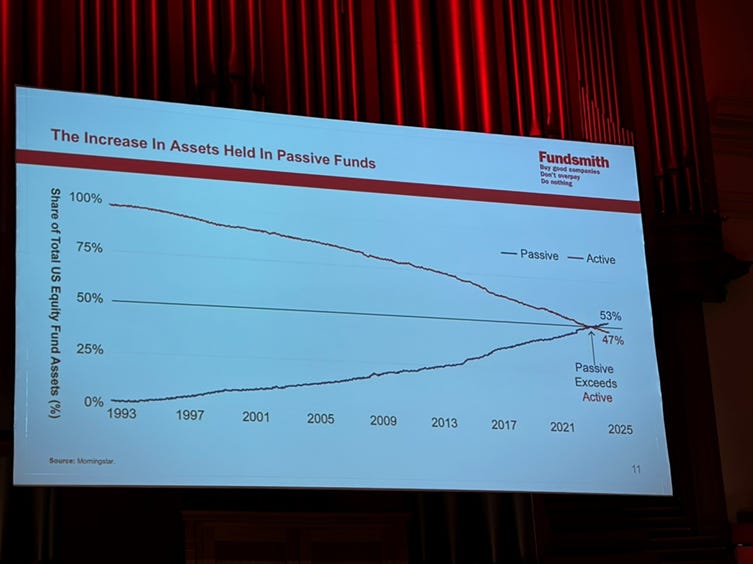

Passive dominance, ETFs, and concentrated leadership have created a market where prices can move violently for reasons that have little to do with the underlying businesses. Passive has now overtaken active in the US:

Passive has Overtaken Active

Source: Fundsmith

The lack of active fund managers to take the other side, the increased concentration of markets and the greater weight of money run by short term operators like pod shops are all contributing to much higher volatility in markets.

Concentration

Smith repeated some of the points he made in his letter – the top 10 stocks were 34% of the S&P500 in 2024 but contributed 63% of the performance (similar to 2022). Concentration last hit that level in the 1920s, just before the 1929 crash. And he made the point that the index is now a momentum fund – when it starts to correct it could fall a long way. And it’s not just stocks – he attributes the run up in bitcoin to the SEC approval of bitcoin ETFs; and when they started to see outflows, the bitcoin price collapsed.

There is probably some truth in that, more than the similar slide he presented showing the run-up in gold which he similarly attributed to the GOLD ETF flows; he didn’t mention that 18 months of $5-10bn of annual ETF inflows weren’t going to move the gold price from $1000 to $5000. I think that argument stretches the data.

The Portfolio

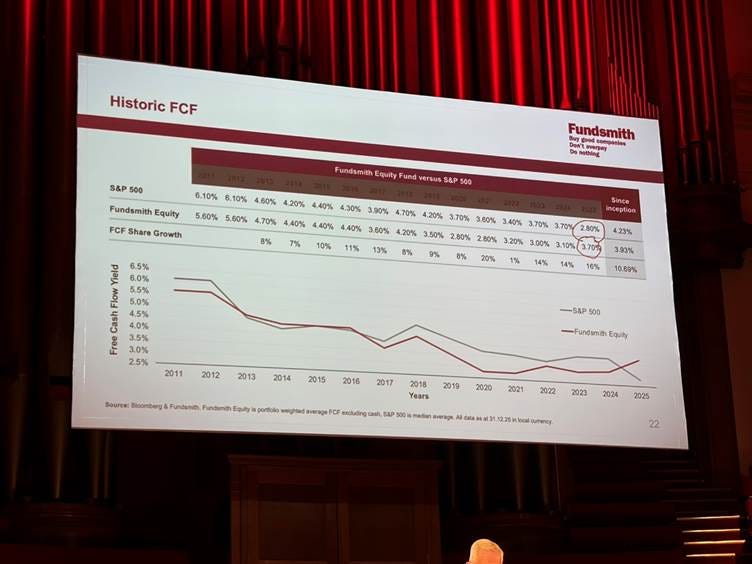

He talked about the portfolio which at the end of last year had a FCF yield of 3.7% which is higher than the S&P500’s level of 2.8% (ex financials), up from 3.1% the prior year partly down to 16% growth. That’s surprising for a quality portfolio earning 30+% returns, more than 1.5x the S&P500’s returns.

Fundsmith Valuation Relative to S&P 500

Source: Fundsmith

He went through some of the portfolio stocks – the winners and losers and the new buys and sells. A few takeaways:

Alphabet –Gemini started 2025 perceived as an AI loser and ended the year seen as a winner. That rapid change is a characteristic he dislikes in his investments.

Novo Nordisk – investing in a drugs company, which he ruled out when he started the fund, was a mistake. The company has been mismanaged.

Church & Dwight has secondary brands which would be expected to do well in a weaker economy, but the K shaped economy isn’t helping them, perhaps because poorer people are doing really badly. That will come back thinks Smith.

Coloplast did two acquisitions and took their eye off the ball in the main business. He will wait to assess the new CEO before making a decision.

Fortinet is a cybersecurity business competing with Palo Alto Networks and is under pressure because of fears that routers may be bypassed, but this looks unlikely – the hardware is an essential element of the security package.

They sold Pepsico and Brown-Forman basically on GLP-1 issues. To own a drinks company, they would need to hear the CEO accept that there is a problem with Gen-Z drinking less and explain what they are going to do about that.

They have made a number of new buys which I highlight below for premium subscribers.

Later he was asked how he selected stocks to sell when he got redemptions and he and Julian Robins, Head of Research, explained:

When a position is close to 10% (European rules on open-ended funds under the UCITS regime cap individual holdings at 10% and aggregate positions of over 5% at 40%);

When the aggregate of 5% positions nears 40%

Valuation

Exiting a sector, eg the drinks sector

Julian made the point that they used to have inflows every day so they could just top up the underperformers. It’s much more difficult to manage a shrinking fund than a growing fund.

Smith concluded his opening section on the performance of the fund by saying that his slide was headed Performance So Far. It’s not about the last 12 months, but the next 12 years. Smith is 72.

The meeting seemed designed to make this point: if you’ve stayed this long, it’s probably too late to sell.

Premium subscribers can read on for

Exactly what he’s been buying and selling

And what that says about how Fundsmith is evolving. I break down the logic trade by trade and say where I agree, and where I don’t.Terry’s stance on AI and how to make money out of it

I unpack how Smith really thinks this plays out, and some opportunities as a result.The stock pick we agree on

Terry and I have both been buying a stock which has collapsed on AI fears but while not totally immune (what is?), its main product is never going to be replaced by AI.

PLUS I’ve been experimenting with AI in research workflows. Learn what surprised me.

Stripe Letter

In their annual letter, John and Patrick Collison report another strong year for the internet economy and that Stripe is benefiting from (and investing into) several big shifts:

faster “winner-take-more” dynamics in markets

businesses launching faster, being quicker to reach significant revenue and often being global-first

rapid adoption of AI and stablecoins.

In 2025, businesses on Stripe processed an astonishing $1.9T in volume (+34% YoY). Stripe remains profitable, even after funding heavy product investment. They made two significant acquisitions in the crypto/stablecoins space which is a big bet for the company - Privy for wallets and Metronome for usage-based billing.

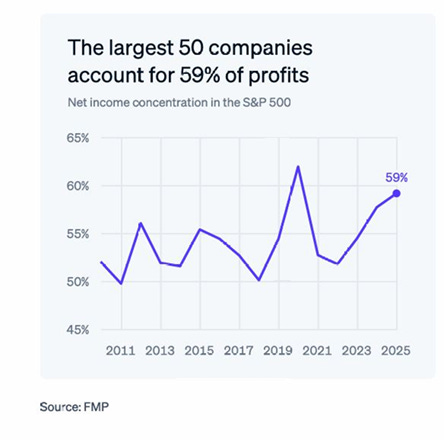

A core theme is that competitive markets are “sorting” faster—more profit and growth are concentrating in leading companies and leading channels, with the profit concentration in the top 10% of the S&P500 being a good illustration:

S&P Profit Concentration

Source: Stripe

The Collison brothers argues this pattern shows up across industries (retail, airlines, healthcare) and is amplified by software/data centre investment and by AI, which is making it easier to start and scale companies quickly. Stripe has positioned itself as building the financial infrastructure for this new era.

One of the interesting points they make is that growth has been constrained by limited access to capital by SMEs since the GFC. They cite bank lending in Ireland dropping by 66% between 2011 and 2019, and small business lending in the UK contracting. In the US, since 2010, loans above $1m are up 68% while loans under $1m are down 5%; only 41% of small business loan applications were approved in the US last year.

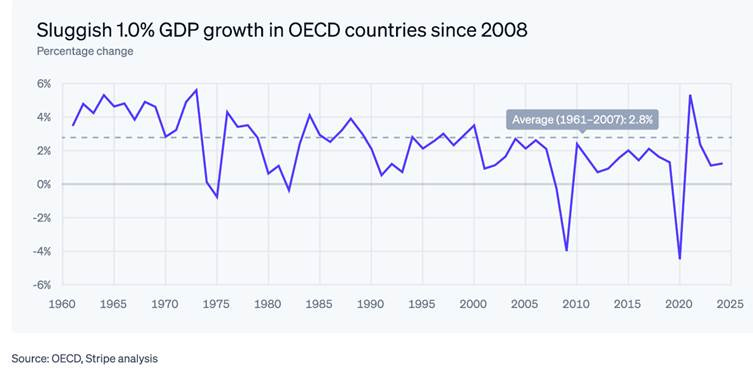

Productivity Growth has Stalled

.

Source: Stripe

Hence they have launched a lending solution and of course they have access to daily revenue data so they have high quality data for lending decisions. Your analyst qualifies, but I haven’t asked the terms.

They also highlight a change in the crypto sphere as stablecoins move interest from speculation to payments, especially B2B; Stripe is working to make global, stablecoin-enabled financial services more practical.

I know everyone is fretting about SaaS companies but the underlying trend of e-commerce is clearly highlighted in the chart and Stripe is a brilliant play.

US Retail Trends

Source: Stripe

Their approach to Paypal and increase in valuation this week to $159bn (+70%) are no surprise – in September, 2021, they were rumoured to be planning an IPO at $250bn the following spring, but markets intervened. I think they will come to the market and I am set to buy – they “own” 3% of my business (or at least this Substack and the internet school) and of a large chunk of the internet. It’s rare to find a company like this.

And a word from my sponsor.

As we enter 2026, the global economy is entering a more fragmented and consequential phase. The focus has shifted from “model bets” to “agent bets” and from hype to measurable ROI. AlphaSense recently released their Top Market Trends 2026 report, a comprehensive sector-by-sector overview of the critical forces shaping the year ahead, powered by insights from AlphaSense.