27 Value Investing Ideas from New York’s Best Minds

Pitches from 14 top investors with 375 years of experience—has value’s time finally come?

I am writing this from my New York hotel room – thankfully this one has a desk. On my last trip, I wasn’t so lucky. And gosh, it’s an expensive place. A (probably ridiculously) wealthy fund manager even complained to me that our drinks (admittedly in the Four Seasons bar) were expensive – not much change from $100 for a gin and tonic and two soft drinks.

I attended the Value Investing Conference and Quality Growth Conference on consecutive days. The events were even better than the London ones (same organiser, better/different speakers). Of course, the proof is in the quality of the ideas and let’s see how that turns out, but I have a lot to write about in coming weeks, and I shall be doing some work on a few of the more interesting ones personally.

This week, I shall cover the Value Conference and next week the Quality Growth conference and then I shall go through two or three ideas each week, as normal.

I shall probably outline 40 stocks in the next couple of months and at $35/mth, that’s under $2 per idea.

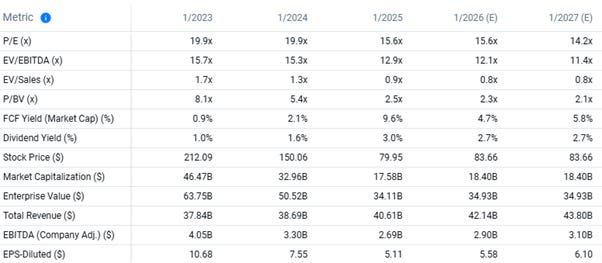

We've reset our strategy to grow shareholder value

We're targeting to grow free cash flow* at more than 20% (CAGR 2024-2027) and deliver ROACE of more than 16% in 2027.

*Adjusted operating cash flow

Key Takeaways

A few themes emerged consistently from the presenters:

The U.S. market is expensive. Many speakers warned of overvaluation in U.S. equities.

International markets offer better value. Europe and Asia featured prominently in discussions.

Value investing is at an inflection point. Multiple speakers argued that value investing is set for a resurgence. I know that the Mag 7 is down 10+% and value is up 10+% in Q1, but the cheerleading made me expect a short term reversal.

Value doesn’t mean buying junk. Many presenters pitched high-quality stocks that happen to be undervalued.

The value-growth divide is more marketing than reality. Some stock pitches at this conference could easily have been presented at the Quality Growth conference the next day. And one of the pitches at that conference was firmly in the value category.

Presenters

David Samra, Artisan Partners

Samra runs a $45bn international concentrated fund and gave an impressive presentation. He ran through one past idea and a similar current idea. He explained his strategy as finding cheap quality stocks with good management and strong balance sheets which are temporarily out of favour. This with the odd variation was a recurring theme from many of the presenters.

Samra pitched a European conglomerate.

Django Davidson, Hosking Partners

Django is a former partner of TCI-backed Algebris Partners and had spoken at the London event I covered last year. He spoke about the capital cycle, a speciality of the firm – Jeremy Hosking was one of the authors of the original Capital Account book. Django is engaged in a marketing drive as they feel that now is the time for value investing to return and they want their clients to come onboard and enjoy the benefit of the inflection.

Again this idea of an inflection point for value was a recurring theme from a number of presenters and is a key takeaway from the event.

Django pitched a sub-sector which is at a capital cycle extreme.

David Iben, Kopernik Global Investors

Dave is the founder and CIO of the firm. He has spoken at the London event in the past and was highlighting that value’s time has come and had a torrent of ideas, all covered very briefly which I shall try to expand on.

Iben pitched a range of stocks, mainly in Asia, including Japan.

Jennifer Wallace, Summit Street Capital Management

Jenny, founder and CIO of Summit Street Capital Management, was up next. She was formerly with the Robert M Bass investment groups and has 30 years of investing experience, a characteristic of many of the speakers. I had been introduced to her in Omaha by Chris Bloomstran who rates her highly.

Jenny highlighted two quality stocks (which I had never heard of) in particular small niches.

Anand Vasigiri, Artisan Partners

Vasigiri is the co-manager for the Artisan International Explorer strategy. He explained in quite emotive terms why he thought the US market was at a valuation extreme and international value’s time had come.

He pitched a high quality Japanese stock.

CT Fitzpatrick, Vulcan Value Partners

I have met CT before in London and he endowed the Fitzpatrick Center for Value Investing at the University of Alabama, where John Heins is the director. You may know him as the publisher of the excellent Value Investor Insight publication which I recommend. John moderated the session and it was good to meet him in person for the first time.

CT explained his process and why patience is so important with an example of an interesting and well-known US stock, whose initial purchase was ill-timed, but which he stuck with and it delivered in the long run.

Bernard Horn, Polaris Capital Management

Horn was a colourful figure in a bow tie. He founded Polaris in 1995 and claims it has one of the longest global and international track records of any firm with the same individuals still managing the money.

He pitched a quality European stock whose valuation has been undermined by a temporary dislocation.

That made it time for lunch which was surprisingly good and unusually healthy and allowed for some decent networking. That allowed me to catch up with some old friends and some clients, including one who had just moved from her firm’s London office.

Andrew McDermott, Mission Value Partners

Andrew has previously presented at this conference in London, has 100% of his portfolio in Japan, and has met the sage, Warren Buffett, who picked his brains on the country.

I think it’s against the rules of the conference not to pitch an individual stock, but I missed his. He did have an interesting discussion on Japan with the moderator David Salem of Hedgeye. I visited the Hedgeye office on the Friday to do a live TV interview with founder Keith McKullough.

Andrew Wellington, Lyrical Asset Management

Wellington is co-founder of the firm and has 25 years of experience. His really interesting presentation pitched 3 of his holdings. He showed a long term chart of earnings progression, his holding against say a Microsoft, then explained that his stock had better earnings growth at a fraction of the multiple. It was persuasive.

Andrew pitched 3 US stocks.

Kim Shannon, Sionna Investment Managers

Kim started in the industry in 1983 and is the founder of Sionna. She was another manager beating the drum for value.

Kim pitched a Canadian large cap.

Samantha McLemore, Patient Capital Management

Samantha is the founder of Patient Capital and took over one of Bill Miller’s funds when he retired, having worked with him for over 20 years. She gave a fascinating presentation on how Miller achieved such an outstanding track record, which I intend to write up separately in coming weeks.

Samantha pitched 2 US large caps.

Jeff Everett, Tectonic Investors

Jeff has 30 years of investment experience and is the founding partner of his firm, which specialises in “identifying and capitalizing on transformative forces shaping global markets”. Maybe there wasn’t room for him at the Quality-Growth conference.

Jeff pitched an intriguing Chinese tech name.

“Fireside Chat”

The day concluded with a fireside chat between Joel Greenblatt on Zoom and Rich Pzena, who founded his eponymous firm in 1995 and runs its US large cap and best ideas strategies. Joel Greenblatt needs no introduction, as he has written several great books, has been an adjunct professor at Columbia and has produced a stellar performance over decades.

Greenblatt has done one of these zoom calls before at the London event and I was slightly disappointed not to be in the same room as him. I have no idea why as its unlikely that his magic is going to rub off on me if we are breathing the same air. I was curious that he appeared to be at home, but there were no paintings on the wall and the bookcase didn’t have a single book. And it wasn’t a minimalist setup.

Pzena and Greenblatt went to school together. I have no idea what they learned there, but it was obviously quite effective. Pzena explained that great businesses don’t sell at low prices. He tries to find stocks where something has gone wrong and the market doesn’t believe that it’s a good business any more. This was a strategy that several of the presenters at both conferences highlighted. He thinks that this is a good way to find stocks that can double or treble and which have limited downside.

Dollar General Stock Price

Source: Alpha Sense

He explained that he liked Dollar General which had fallen from $250, bottomed in the $70s and is in the $80s now. It has more US locations than any other retailer and caters to the low income customer.

Margins have halved thanks to a number of unforced errors:

They messed up the inventory in Covid

Labour became an issue in Covid

Shrinkage became a problem

Dollar General Valuation

Source: Alpha Sense

He bought the stock at 11-12x P/E and it’s now at 13x. Margins are half the long term average. He highlighted the stock’s 6-7% FCF yield if they don’t turn it round and sees a home run if they do.

Dollar General Estimates Trend

Source: Alpha Sense

As ever with these situations, the issue comes down to the estimates – have they stopped falling? I have no idea how tariffs will affect the stock, but it may well be quite defensive and economy neutral, given the customer demographic.

The stock is popular with value investors. Two of my podcast guests, Chris Pavese and Chris Bloomstran own it and referred to it in their investor letters:

Here is Chris Pavese of Broyhill:

“Shares of Dollar General lost 36% in Q3. Dollar General has historically proven to be a safe haven for investors in uncertain times as consumers trade down and increase their spending with the retailer. While inflation has certainly put pressure on DG’s core customer in recent years, the retailer has seemingly lost market share to larger competitors.

The most recent earnings report highlighted this dynamic, contrary to our expectation for a weaker economic environment to benefit the company.”

Chris Bloomstran wrote 7 pages on the stock – extracted here. It’s pretty comprehensive, as I have become accustomed to with Chris and he is an outstanding analyst. I thought this was a key comment in his analysis:

“The typical customer will shop at a Walmart or larger town supermarket on weekends. During the week Dollar General is often the only game in town, selling items at roughly a slight 1.5% premium to Walmart on a price per ounce or common-size equivalent basis. Where competition exists it’s often a convenience store or drug store where prices to the customer are 20% to 40% higher.”

This is what David Katz wrote in the Matrix Large Cap Value Strategy:

“Dollar General operates over 20,000 discount stores in 48 states. The company’s customers are largely lower income budget conscious consumers who are attracted to the stores’ low prices, wide assortment of goods, and convenient locations, particularly in rural areas where other retail options may be limited. The company’s share price reached a multi-year low after a series of earnings disappointments and lower earnings guidance. We believe the company is in the early stages of executing a plan that will return it to a path of earnings growth and better stock performance.”

But not everyone is as enthusiastic, pretty obviously given the share price – here is one counter argument from Ward Kruse who runs Coho Relative Value Equity:

“…we eliminated our Dollar General (DG) position during the quarter. DG had been a consistent operator through most of our nearly nine-year ownership up to and through the COVID pandemic. Following the pandemic the company began to experience operational issues that started within the supply chain and led to disruptions at the store level. We viewed these as operational issues, that while unfortunate, could be corrected in time particularly once Todd Vasos, the architect of tremendous shareholder returns through the majority of ownership, returned as CEO.

In accordance with our Position Paper discipline, we were monitoring several items to gain confidence that progress was being made and that growth would resume. We understood fixing a supply chain, improving in-stock levels, and reducing shrink do not happen overnight, and it would take multiple quarters to return to the desired level of performance. That said, the initial signs were more encouraging than we expected. On-time and in-full truck deliveries were fixed within weeks. This led to a more rapid improvement in in-stock levels than we had assumed. The company also returned to positive traffic growth several quarters ahead of our expectations which helped drive above-consensus, same-store-sales performance for three consecutive quarters.

There was an abrupt shift in that same-store-sales cadence in the second quarter of 2024 with store traffic disappointing. To us, this signaled that the progress being made operationally was insufficient to overcome what we now believe are underlying structural issues with the dollar-store industry more broadly. To address these structural hurdles, we believe DG will need to invest more in price, labor, and store standards to improve the shopping experience for customers and to sufficiently convince those consumers of the value and convenience proposition relative to competitors like Walmart and Amazon.

The extent, length, and breadth of those investments are difficult to forecast and led to the sale of the position from the portfolio.”

The Pzena-Greenblatt session was a fascinating conversation and I shall go into it in more detail in coming issues. Premium subscribers can read on for a list of the stock recommendations and if that isn’t worth $35 (which doesn’t even buy you a glass of wine in the Four Seasons bar), then I don’t know what is. I am really excited at what I shall be writing about in the next couple of months and I am hoping many of you will join for this exciting journey.