Is the Consensus Wrong?

Featuring a major issue the sellside has missed

Background

It’s that time of year – New Year Resolutions are made, the gym fills up for the first two weeks of January and the smart money takes stock of what they got wrong last year and makes a plan for the year ahead. (If you would like a good template for your New Year’s Resolutions, you are in luck if you are a paying subscriber – link at the end.)

One of the features of the turn of the year in the investment world is the proliferation of new year predictions on the economy and year-end market levels.

I have never paid much attention to GDP estimates or predictions for the S&P500. I generally focus on the direction

of economic growth (accelerating or decelerating)

of earnings forecasts

But we are at an unusual juncture in markets and economies and an understanding of the economic picture is essential to guide positioning in markets. To that end, I have undertaken the slightly painful task of reading a larger than usual number of 2023 outlooks from the big brokers and asset managers. Here’s what they say and what I learned:

The Economist’s annual Year Ahead uses the forecasts from Good Judgment which predicted global growth probabilities as:

2023 GDP Growth Forecasts

Source: Good Judgment via The Economist

And here is Deutsche Bank on Bloomberg consensus inflation estimates:

Consensus Inflation Estimates

Source: Bloomberg via Deutsche Bank

The consensus estimate for GDP growth in the US is 0.4%, which is a massive slowdown, but there is a huge variance among forecasters. Using a Wall Street Journal Survey of 66 economists in October, 2022 (full results are in a spreadsheet for paying subscribers), I estimate that range as -1.6% to 3.3%, which is obviously extremely wide. They also asked for a prediction of the likelihood of recession which is really high by historical standards:

Probability of a US Recesssion

The WSJ headline “Economists now expect a recession“ in the US in 2023 was based on a consensus of modest negative growth in Q1 and Q2, and then a positive Q3. This is a sharp slowdown but the stockmarket has already anticipated this result.

Here are 2023 S&P 500 targets from a range of forecasters:

23 S&P 500 Targets

Source: Francois Trahan

As I write, we are at 3853, so only 3 are predicting a down year. That’s probably 3 more than usual. The consensus is 6% up.

This is what Barclays had to say about 2023:

Barclays

The macro environment is not encouraging heading into 2023. There is no end in sight to the war in Ukraine. Europe faces further energy headaches next year. China is growing almost as slowly as in pandemic-affected 2020. US housing activity has collapsed. And inflation has forced Western central banks into a dizzyingly fast pace of hikes. Three themes are front of mind for Barclays Research analysts:

1. Next year will be a long, hard slog

2023 may well be one of the slowest years for global growth in decades. Barclays analysts expect the world to grow at 1.7% next year.

2. Major central banks will remain restrictive even as economies contract

The data that really matter are not cooling quickly enough, despite the latest CPI report, and they emphasise that a pause is not a pivot.

3. Barclays Research analysts are negative on risk assets, for a fourth straight quarter

US stocks tend to bottom out 30-35% below peak in the middle of a recession. That suggests fair value of 3200 on the S&P500 sometime in H123. European valuations look more reasonable, but that is offset by a considerably worse macro outlook than in the US.

I started with Barclays as this seems pretty close to the consensus view and the one thing we know about the consensus is that it’s unlikely to play out as telegraphed. Incidentally, I noted more than one bank’s prediction for 2023 as being

“better than 2022”

This could be anything from -19% to +19%! Here are some other findings in no particular order.

Morgan Stanley IM

This is not the sellside powerhouse but there is some genuinely useful material here, particularly from Counterpoint Global:

Impact of a higher cost of capital on the competitive landscape:

“With the days of easy money behind us (for now), we expect fewer market entrants and less competition, which should benefit companies that have already established valuable businesses and brands.”

“Stock-based compensation plans have been a low-cost funding mechanism for emerging and innovative businesses. Given the recent drawdown, we are monitoring whether companies will increase the use of cash compensation and any subsequent impact on profitability and dilution”.

I thought these were two important, second order thinking, points. They are obviously in opposite directions, which seems to be a characteristic of the 2023 outlook – there are often forces pulling in different directions which clouds the outlook.

MSIM flags two bullish signals:

1 Broader breadth in the S&P 500 (as illustrated by the equal weighted index (-11%) outperforming the S&P 500 market cap weighted (-17%).

2 Sectoral leadership: financials, industrials and materials have performed well while brokers and banks have been ok, suggesting the market is bullishly inclined.

The stockmarket is the most reliable prediction tool and this positive market bias is important to note.

They expect the US economy to be very resilient and earnings to drip down slowly, frustrating the bears.

They like companies with pricing power and recurring revenues – high quality compounders – consumer brands, software, healthcare. Have seen valuation compression.

Main risk is earnings. “ However, with forward earnings expected to rise over the next year and margins close to record levels, we do not see earnings signaling a significant economic slowdown, let alone a serious recession.”

I am not clear why they expect forward earnings to rise, especially given margins at record levels.

Risk of higher tax rates.

This is a really important issue and I would be wary of companies with low tax rates.

Time for emerging markets to shine in the next decade

They like high quality EM growths tocks with 15-20x P/E, 20% ROIC and 20% eps growth.

I haven’t done the screen but I would be surprised to find many of these.

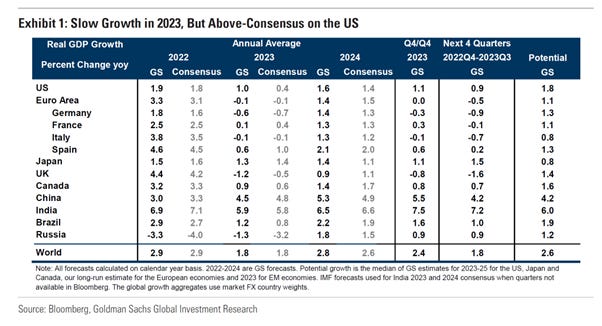

Goldmans

Global growth of 1.8% in 2023 – US resilient, Europe in mild recession, China reopens

US inflation to fall to 3%, rates to peak at 5-5.25%

More bullish than consensus on the US as current data not that weak, real personal disposable income rebounding, and don’t expect much more tightening to come.

The Goldman view of the US outlook is almost goldilocks, but it’s certainly feasible.

Goldmans and Consensus GDP Growth Forecasts

Sources: Goldmans, Bloomberg

KKR

More constructive tilt especially on parts of credit

Equities – smaller value oriented plays rather than larger cap tech

Weaker dollar

Capital markets new supply (i.e., new issuance), a proxy for calling bottoms, has dwindled essentially to nothing.

The chart below is certainly bullish – it would be interesting to see demand stats, eg corporate buybacks and retail investment into ETFs for example. I am working on this.

New Issuance

Source: KKR

Citi Private Wealth

No bear market has bottomed before a recession has begun.

This is an important point, although not a rule.

Nevertheless they suggest you put excess cash to work.

They like defensive equities and dividend growers (looking not only at yields but FCF cover and payout ratios)

The Attraction of Dividends

Source: Bloomberg via Citi

They like energy transition plays, for example renewable energy technology, energy storage, electric vehicles, heat pumps, sustainable materials and carbon capture.

We all like these things, but try investing in say, carbon capture – hardly a wide range of publicly quoted options. A number of firms echo the dividend point, for obvious reasons.

UBS AM

Diversify beyond 60:40 with exposure to real assets and a wider selection of fixed income markets

Fixed income now offers positive yields

Long-short strategies should provide alpha

Credit Suisse

2023 is likely to be challenging

Diversify investments broadly

Inflation is peaking but will remain above central bank targets

In equities, prefer sectors and regions with stable earnings, low leverage and pricing power now.

Will rotate towards interest rate sensitive sectors later (good luck with timing that!)

Like long duration Treasuries, EM hard currency debt and investment grade credit

See real estate as more challenging

Deutsche Bank

Easing but continued inflation and mid single digit equity returns

High quality bonds have decent yields which could compensate for rate rises

Earnings will not fall in nominal terms

Prefer cyclicals and value stocks to expensive defensives

Asia is the most attractive region

GDP Outlook

Source: Behind the Balance Sheet from Deutsche Bank forecasts and Microsoft data

A neat, new (at least to me) feature in Excel was that the countries could be converted to a data table and then data like population and GDP added.

Equities with Reasonable Valuation

Source: Deutsche Bank

Here are their targets for end of 2023, some quite bullish.

Deutsche end-2023 Targets

Source: Deutsche Bank

BNP Paribas

On brink of recession and equities will struggle to do well

Prefer US growth to Europe where v cautious

Investment grade credit attractive in fixed income

Also like private infrastructure debt

Sustainable recovery theme eg green infrastructure

China cheap but rerating unlikely

BNP are an outlier in their negativism

JP Morgan AM

Bad year for economy, better year for markets

Inflation to moderate

Stocks and bonds look attractive

Prefer value to growth

Earnings estimates only -5%, should be -10 to -20%

Stocks may fall further but have priced in some of the likely earnings downgrades and will be higher end-2023

Like stocks with dividends

Fidelity

Deteriorating environment not yet reflected in equities

Expect a high degree of volatility and uncertainty for global equities in 2023

Defensive areas such as financials and utilities could outperform as the economic slowdown takes hold

Bond yields are finally starting to look attractive again

Consensus Earnings Forecasts

Source: Fidelity

Byron Wien’s Ten Surprises

I love that Byron Wien, now in his 90s, surely, continues to produce this report. He predicts 10+ surprises, which he defines as an event which the average professional investor would assign a one-third chance of taking place, but which he believes has a 50% or better chance of happening. He also reviews his performance for the past year – that’s really unusual.

I like his approach as it forces you to think what might happen. These ideas were my favourites:

Real interest rates turn positive

Margins are squeezed in a mild recession (not sure that this is a surprise)

Market reaches a bottom by mid-year and begins a recovery comparable to 2009.

Nobody has really been talking about the potential for positive surprises – an end to the war in Ukraine or a recovery in China are two possible examples which would be positive for markets.

Modern Monetary Theory is fully discredited because deficits have proven to be inflationary.

US dollar stays strong against major currency pairs.

I encourage you to read the full report. Wien has been a strategist longer than almost anyone and he is full of wisdom – I saw him speak a few years ago and I am delighted that he is still working and sharing his wisdom.

Saxo’s Outrageous Predictions

I also always like Steen’s take on the year ahead. My favourite was that “Gold rockets to USD 3,000 as central banks fail on inflation mandate. As markets and central banks realise that the idea that inflation is transitory is wrong, and that prices will remain higher for longer, gold is sent through the roof, hitting a price tag of USD 3,000”. This is not outrageous in my view.

Less likely, but still a potential risk is “Tax haven ban kills private equity: With the war economy comes an increased focus on national interests and sovereign nations' ability to assert themselves. In that regard, the OECD countries turn their attention on tax havens and pull the big guns out, banning them altogether.” I think that Governments will be forced to claw back some of the past reductions in corporate tax rates.

Earnings Forecasts

Francois Trahan points out that bear markets end when a trough in earnings (EPS) is on the horizon:

Earnings Drive Stock Prices

Source: Trahan Macro Research

He flags that earnings and GDP are tightly correlated across time and thinks that we will have to wait for a recovery in the economy before we can start talking about a renewed bull market. But note that consensus is for a mild and short recession in the US.

Yardeni’s data on S&P500 consensus forecasts is 219.5 for 2022, 229.8 for 2023, a 5% increase and 253.6 for 2024, a 10.3% increase. The trend is shown in the chart:

Consensus Earnings Estimates

Source: Yardeni Research

We start from record margins and inflation will surely induce margin compression so my instinct is to assume that these data are far too ambitious. Although past experience has exhibited a wide range of earnings outcomes in a recession. The impact of inflation on revenues, however, could result in the nominal earnings outcome being better than the napkin maths might suggest.

Persistent inflation of course would be negative for sentiment and there is quite a lot of hope riding on the Fed pivot which seems highly unlikely to this analyst.

Summing Up

My main criticism of this exercise is that it’s all very well saying you want stocks with stable revenues, pricing power and good management,, ideally family owned, but try finding one at a sensible valuation – that is not quite as straightforward.

ESG appears in most publications with two main themes: the energy transition and infrastructure. Few spell out how they will make money though.

One high conviction takeaway is to avoid stocks with low tax rates.

So, what should we conclude? Paying subscribers can read on for

My conclusions

The crucial issue the brokers and banks have missed

That new year’s resolution template

Links to all of the reports highlighted above

Links to the spreadsheet of economist forecasts

I am continuing to give free subscribers access to a significant amount of hopefully high quality content, but my objective is to increase the number of paying subscribers. Thanks for reading.